The Ghost Bomb Six {No.6}

ILLINOIS ... 2020 Early Spring Deaths, Astronomical Investment Gains in 2021 & Unexpected Mortality After the Vaccine Rollout

If you have been following along in this series then you know that this is the final installment of the Ghost Bomb Six.

.

If not, then for any new readers I will do a little refresher of this project:

In this recent post I laid out the parts of a little puzzle I am working on.

In the spring of 2020 there were some places in this country that saw very unseasonal increased mortality.

In the following year (fiscal year 2021) many of these same places had huge windfalls in their public employee pension plans due to historic investment gains.

These investment gains were happening simultaneously with additional increased member mortality into 2021 and beyond.

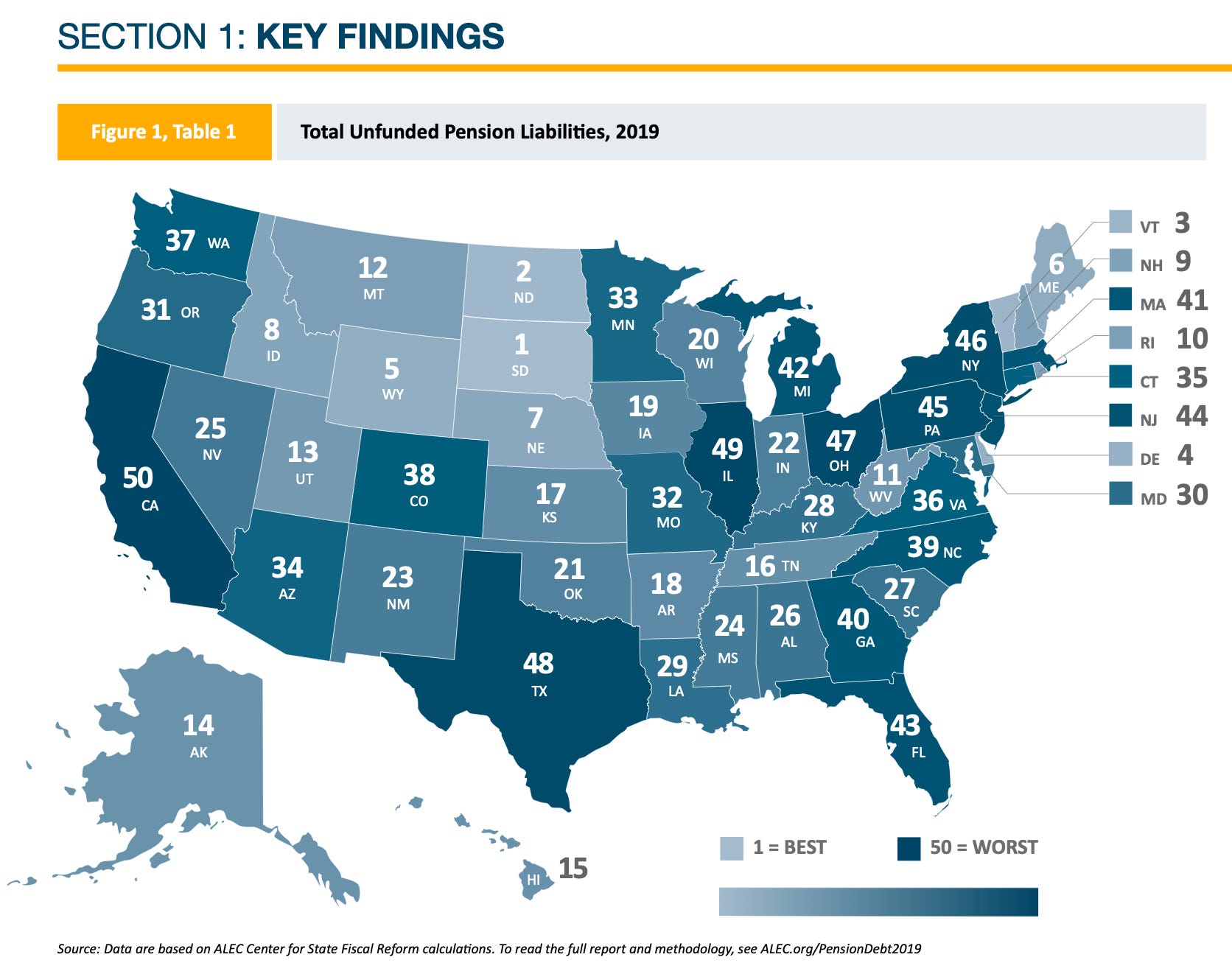

A look back at the solvency of these same pension plans in 2019 shows that many of these locations that had the strange 2020 spring death surge were in pretty bad financial shape right before the pandemic hit.

.

Previously I pointed out that in the 14 US state locations that saw this big spring mortality spike, there were six that also showed up in the bottom ten of the worst pensions of 2019.

Since I have dubbed that April/May death surge the “Ghost Bomb,” these places are now the Ghost Bomb Six.

They are (links provided to the ones we have previously looked at):

Massachusetts … The Ghost Bomb Six {No.1}

Pension System Rank: 41

Michigan … The Ghost Bomb Six {No.2}

Pension System Rank: 42

New Jersey … The Ghost Bomb Six {No.3}

Pension System Rank: 44

Pennsylvania … The Ghost Bomb Six {No.4}

Pension System Rank: 45

New York … The Ghost Bomb Six {No.5}

Pension System Rank: 46

Illinois

Pension System Rank: 49

.

The pensions are ranked with 1=best, and 50=worst.

.

As you can probably surmise from looking at the list, we are doing these in order based on their pension rank according to ALEC. What is ALEC? Good question, and I should have discussed this earlier. I am learning more and more as I go further down this rabbit hole - it seems there are several groups out there that rank pensions, not just ALEC.

ALEC stands for the American Legislative Exchange Council.

From the linked report:

About the American Legislative Exchange Council

The Unaccountable and Unaffordable 2019 report was published by the American Legislative Exchange Council (ALEC) as part of its mission to discuss, develop and disseminate model public policies that expand free markets, promote economic growth, limit the size of government and preserve individual liberty. ALEC is the nation’s largest nonpartisan, voluntary membership organization of state legislators, with more than 2,000 members across the nation. ALEC is governed by a Board of Directors of state legislators. ALEC is classified by the Internal Revenue Service as a 501(c)(3) nonprofit, public policy and educational organization. Individuals, philanthropic foundations, businesses and associations are eligible to support the work of ALEC through tax-deductible gifts.

.

After a little more research into this tangent, it seems that even though ALEC describes itself as non-partisan, many sources you run into may dispute that characterization and paint them as conservative or right leaning. Does that matter a hill of beans? Not sure, but there does seem to be some methodological differences in the various sources of pension rankings.

The reason I am risking boring you to death on this detail is that this almost dead last pension rank (#49) for Illinois from ALEC, actually becomes the very worst if you go out and look elsewhere.

So we are ending the Ghost Bomb Six series here with potentially the most horrible pension system in the country (ALEC was being nice there.)

Sorry California you don’t get that prize after all.

.

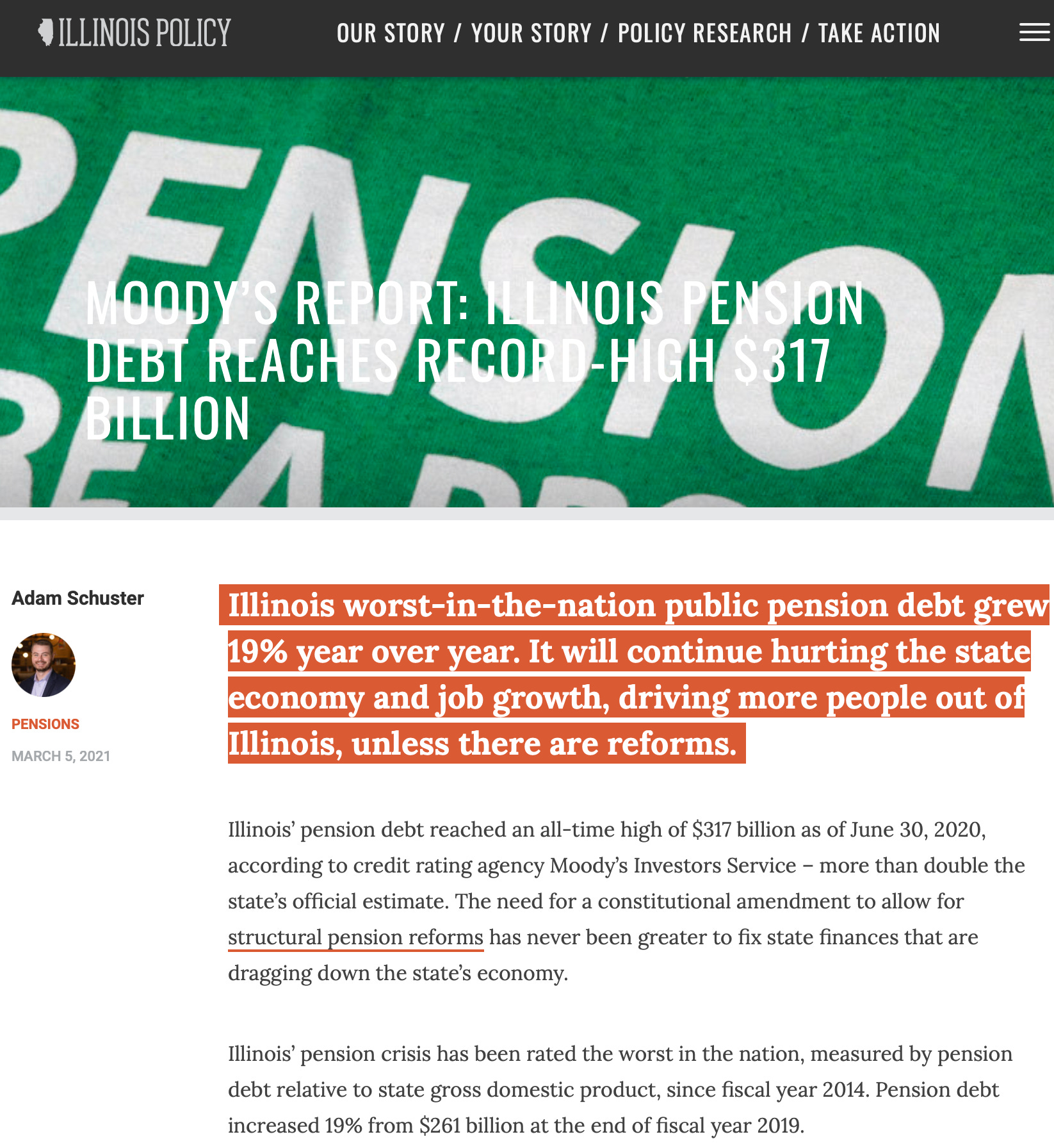

March 5, 2021

“Illinois’ pension debt reached an all-time high of $317 billion as of June 30, 2020, according to credit rating agency Moody’s Investors Service – more than double the state’s official estimate. The need for a constitutional amendment to allow for structural pension reforms has never been greater to fix state finances that are dragging down the state’s economy.

Illinois’ pension crisis has been rated the worst in the nation, measured by pension debt relative to state gross domestic product, since fiscal year 2014. Pension debt increased 19% from $261 billion at the end of fiscal year 2019.”

.

I have come to understand that besides ALEC there are other pension rankings from reputable places such as Moody’s, as we saw in that news story I just linked to.

But there are others … like the Pew Charitable Trust and even the Federal Reserve. I will have more to say on that another time.

Because if you do look at some of those other rankings, then we may have to expand the Ghost Bomb Six to a bigger number - at least to seven.

Like I said, another time.

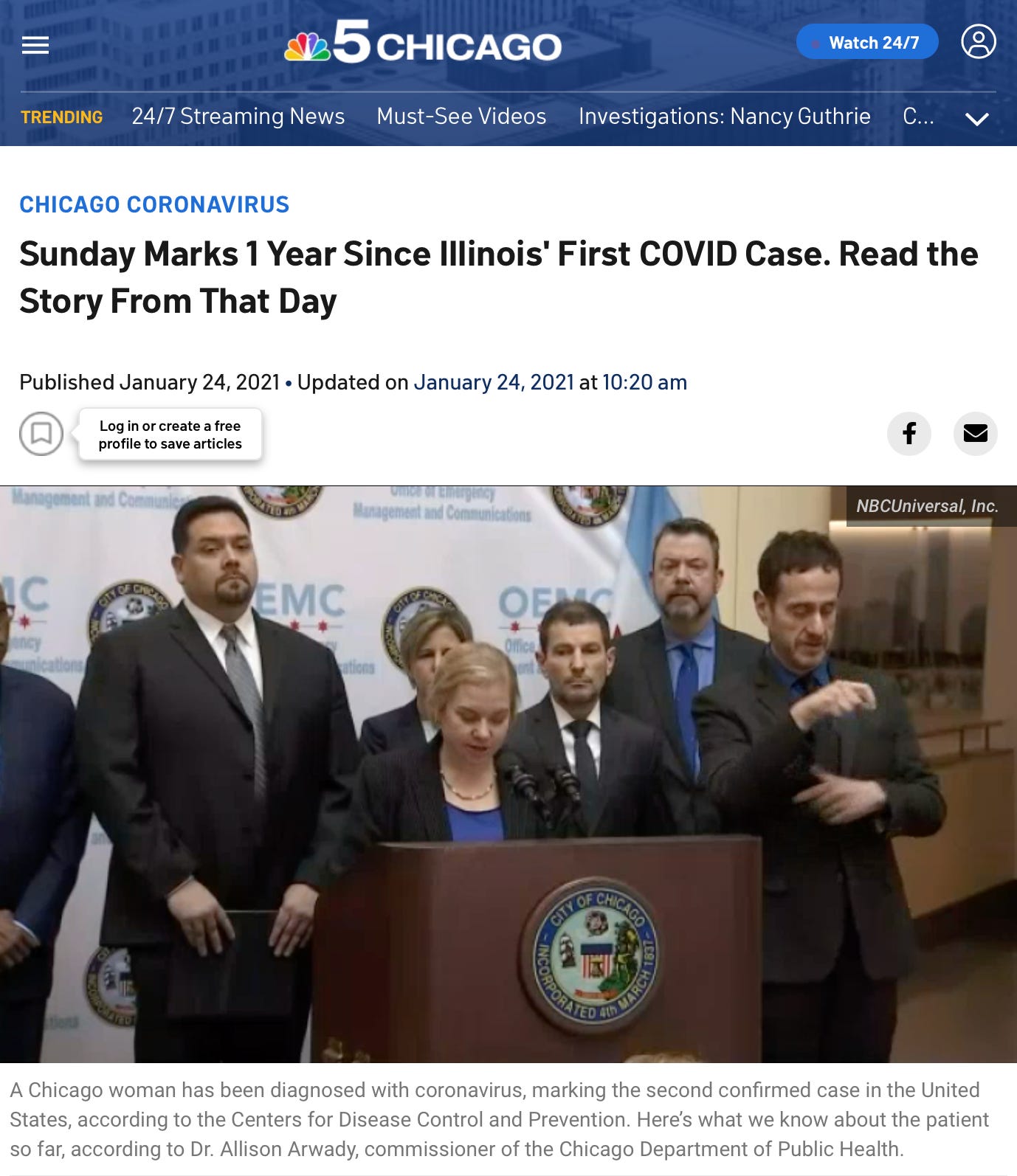

Did you know that Illinois had a confirmed case of covid way before New York?

.

In fact, Illinois had one of the very first in the country.

.

.

.

January 24, 2021

“… This story was first published on Jan. 24, 2020. It marked the first known coronavirus case in Illinois and the start of what would inevitably become a deadly and historic pandemic.

Take a look back at the story as it was written by NBC Chicago exactly one year ago.

A woman has been diagnosed with coronavirus in Chicago, marking the second confirmed case of the new and potentially deadly virus in the United States, according to the Centers for Disease Control and Prevention …”

.

Wow … the second case in the entire country. I did not know that.

Oh well, you can’t be number one all the time. Good job state of Washington!

.

But wait, this just in, Illinois did get a first place covid prize in January of 2020 after all.

.

January 24, 2022

“… Illinois milestones:

January 24, 2020 –First confirmed Illinois case of COVID-19 reported in a Chicago resident, a woman in her 60s who returned from Wuhan, China on January 13, 2020.

January 30, 2020 – second confirmed case of COVID-19 in Illinois reported in a man in his 60s and the spouse of the first confirmed case in Illinois. This was the first person-to-person spread of the virus in the United States.

February 11, 2020 – IDPH announces it is able to conduct testing for SARS-CoV-2 making Illinois the first state to be able to perform in-state testing.

March 17, 2020 – IDPH announces the first COVID-19 death in Illinois.

December 15, 2020 – First COVID-19 vaccines administered in Illinois.

Vaccination is the key to ending this pandemic. To find a COVID-19 vaccination location near you, go to www.vaccines.gov.”

.

First “person-to-person” spread of the virus gold medal goes to Illinois!

.

.

.

The Big Payday

The three largest Illinois state pension systems by assets and membership are:

Teachers’ Retirement System (TRS)

State Universities Retirement System (SURS)

State Employees’ Retirement System (SERS)

.

.

.

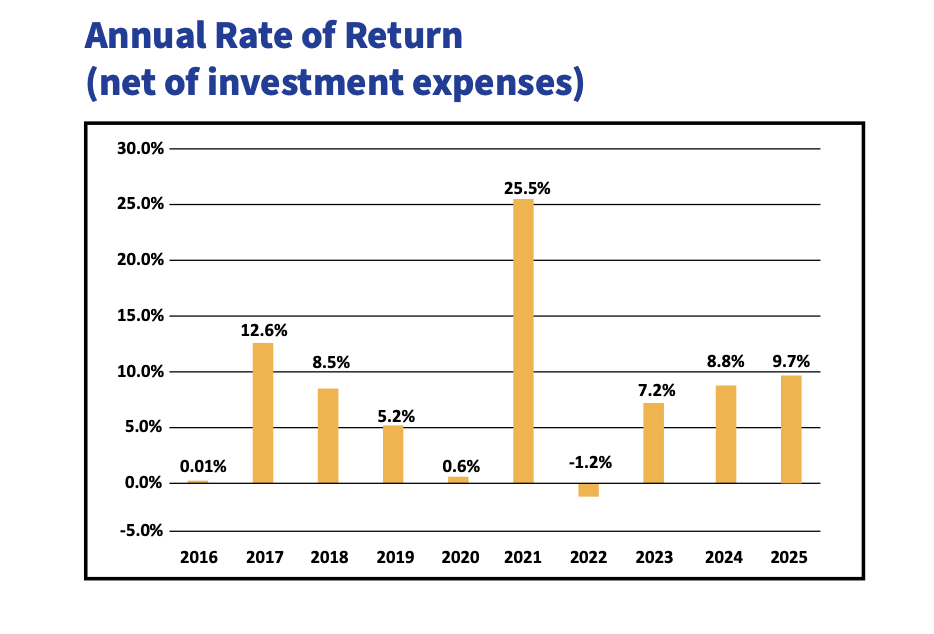

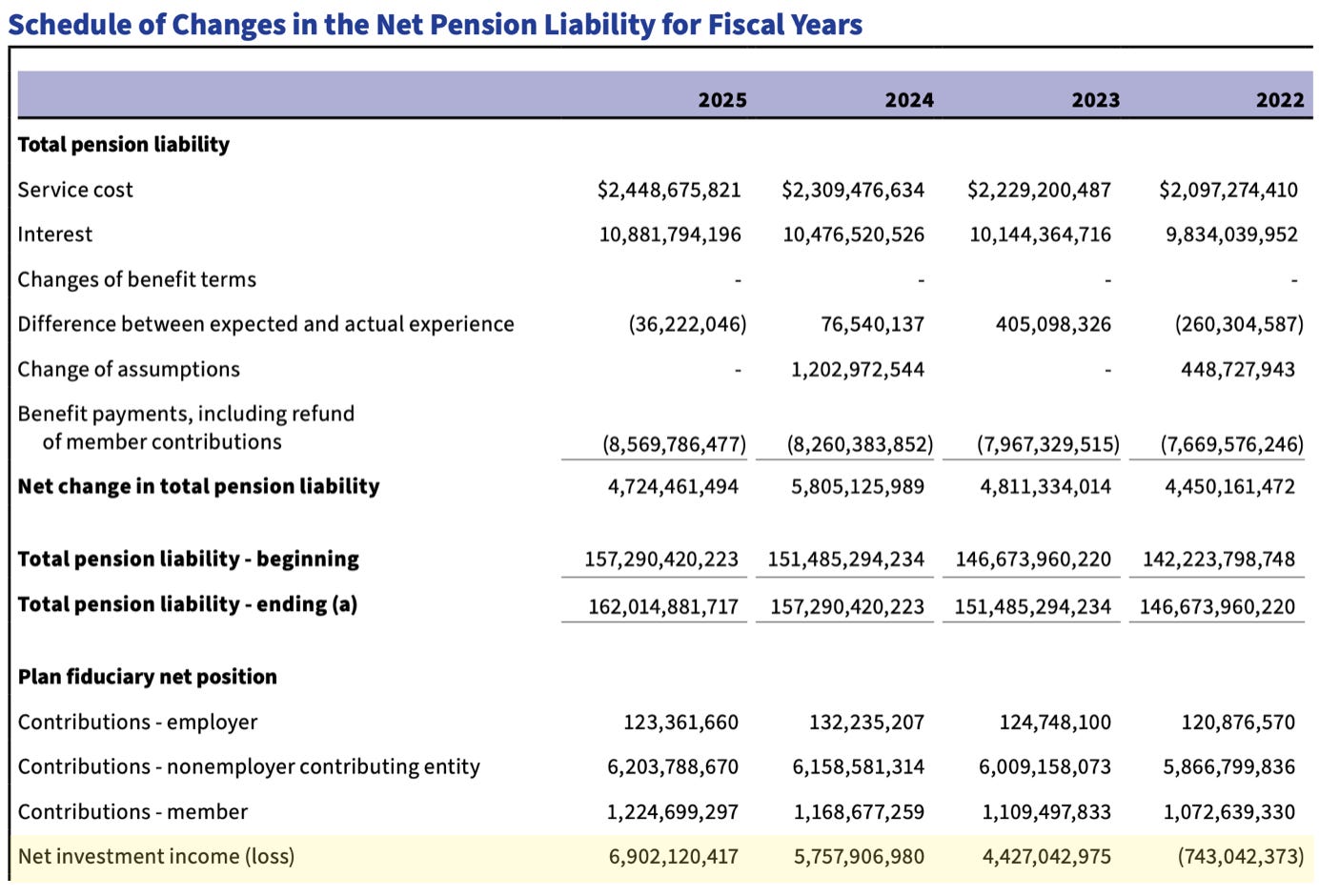

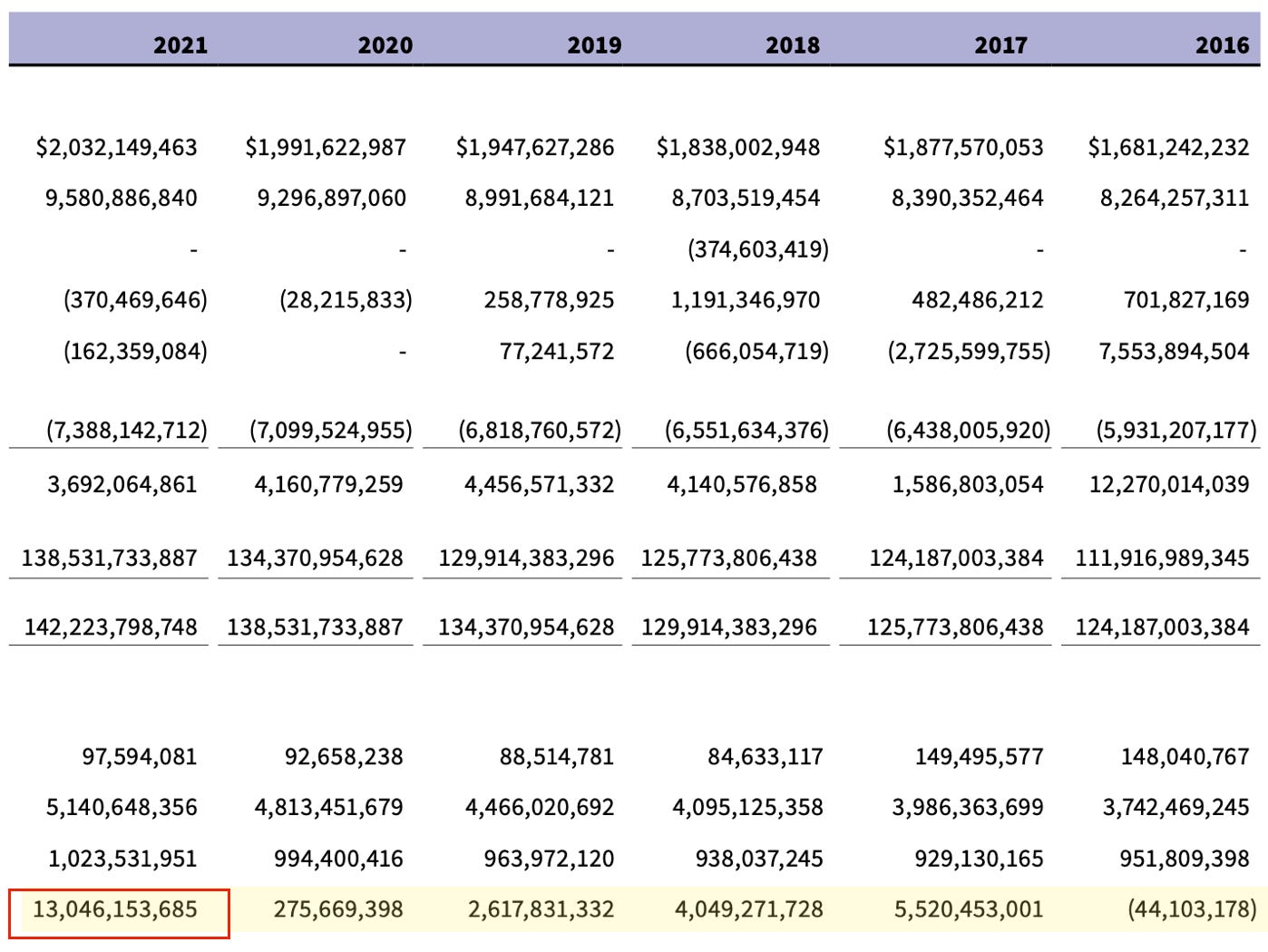

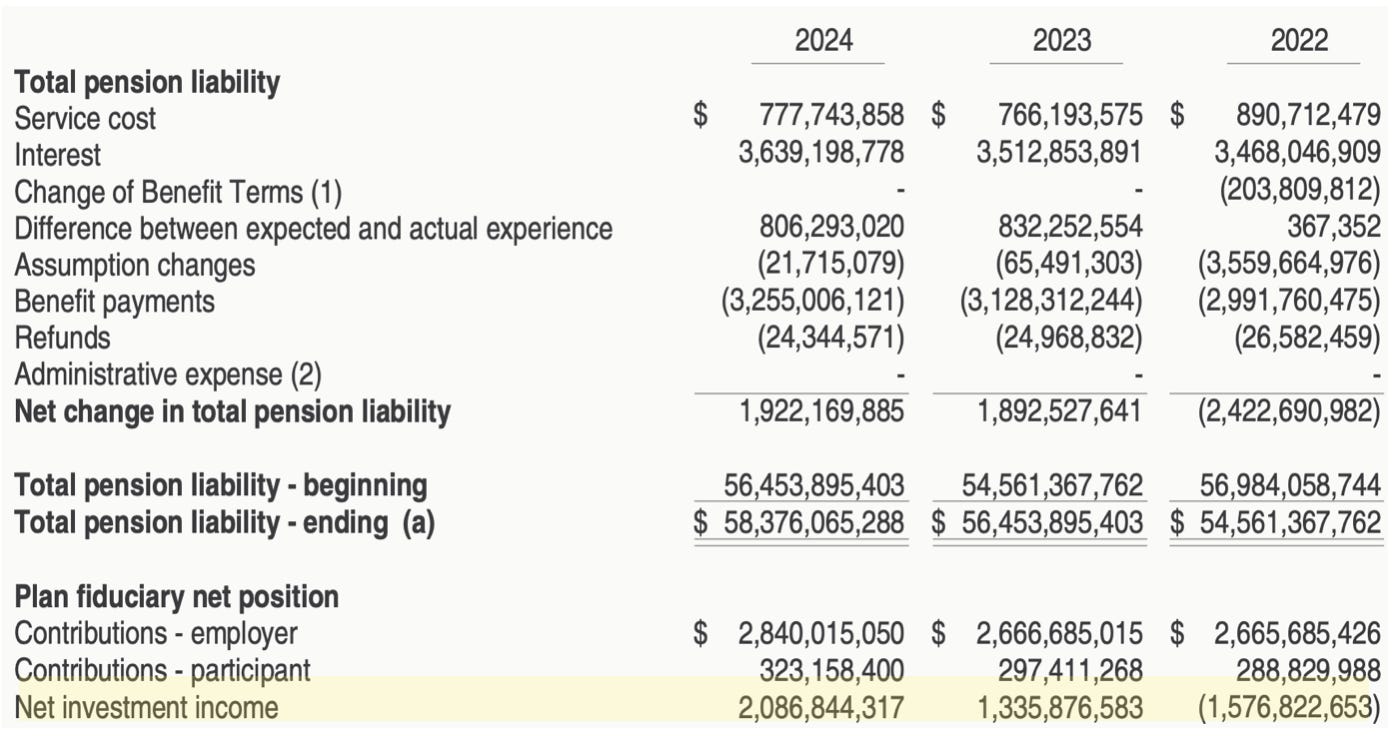

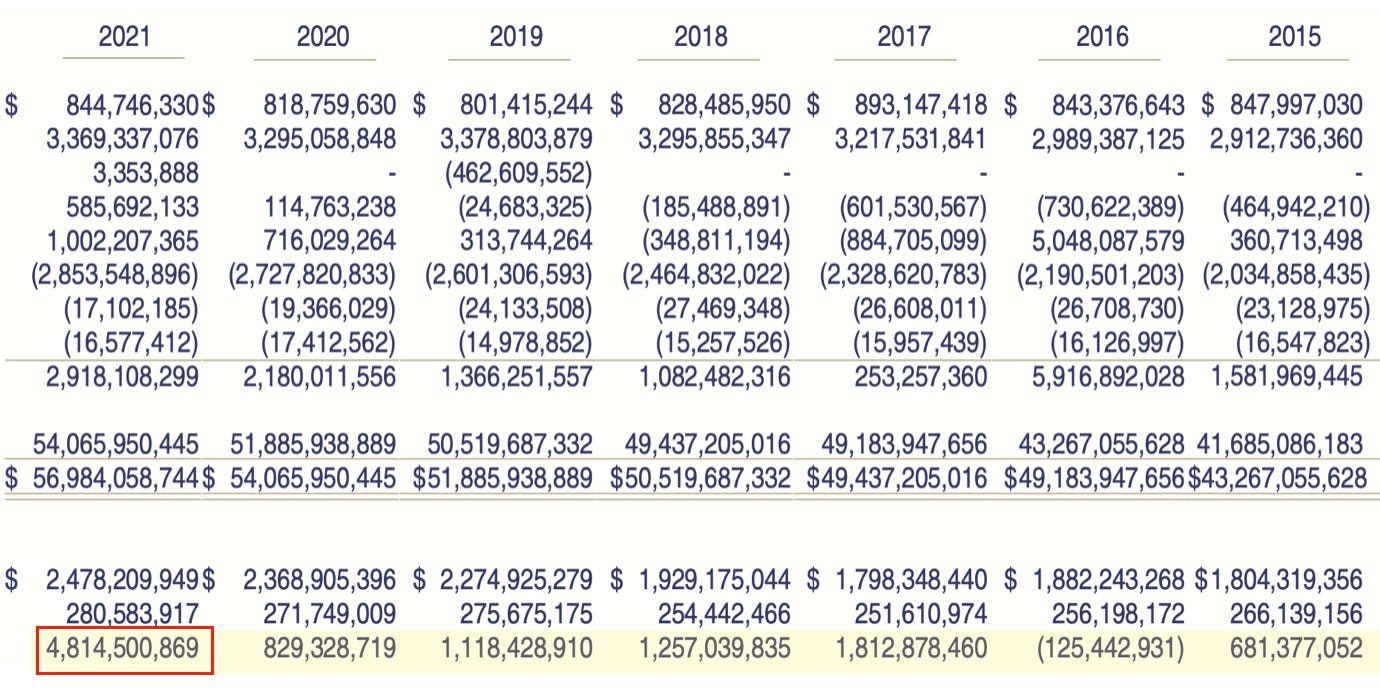

Teachers’ Retirement System (TRS) 2025 Annual Report

.

page 22

pages 54 & 55 (Schedule of Changes in the Net Pension Liability for Fiscal Years)

.

That is an almost 13 billion dollar swing from 2020 to 2021 on the investment gains for the TRS!

.

.

.

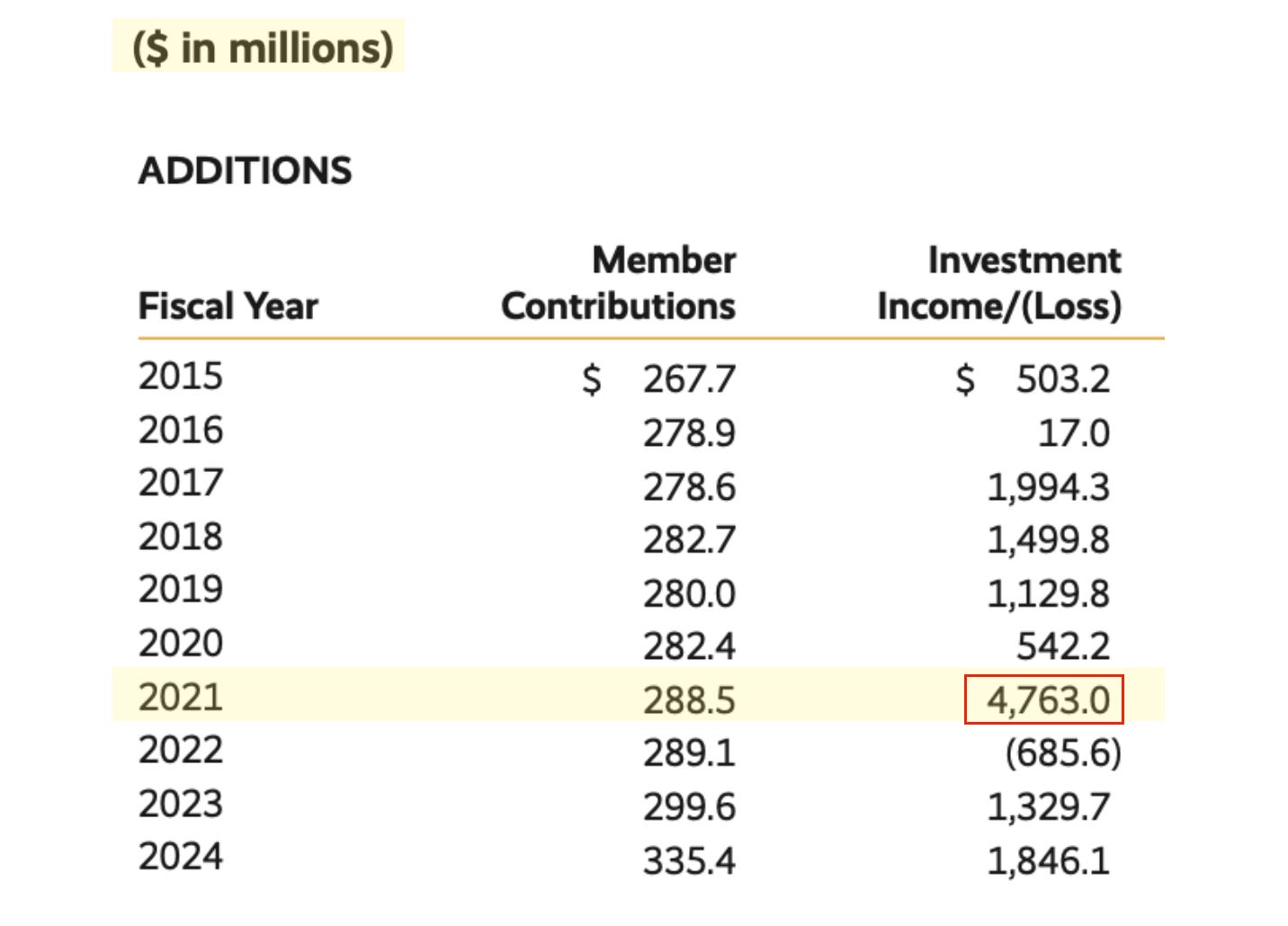

State Universities Retirement System (SURS) 2024 Annual Report

.

page 96 (Changes in Fiduciary Net Position - Defined Benefit Pension Plan 10-Year Summary ($ in millions))

.

That would look to be a bit over a 4 billion dollar swing from 2020 to 2021 for the SURS.

The rate of return for this excellent year was 23.8%.

(source, pg. 29)

.

.

.

State Employees’ Retirement System (SERS) 2024 Annual Report

.

pages 42 & 43 (SCHEDULE OF CHANGES IN NET PENSION LIABILITY AND RELATED RATIOS)

.

So, reading that small print there … looks like the SERS got almost exactly a 4 billion dollar swing from 2020 to 2021 on those investments.

.

page 46 (SCHEDULE OF INVESTMENT RETURNS)

.

.

.

So here it is in a nutshell:

25.5% for the TRS.

23.8% for the SURS.

26% for the SERS.

.

Consistently pretty damn good across the board, wouldn’t you say?

.

Well my good buddy Chat says so. Reader’s Digest version here (look to the supplemental section at the end of this post for more):

Big Picture

Across all three funds:

Typical long-term assumed return: ~6.5–7%

Typical annual range: roughly –10% to +15%

FY2021: ~24–26%, which is 3–4× the assumed return

This happened because FY2021 followed:

the COVID-19 market crash in March 2020, and

a massive global equity rebound in 2020–2021.

✅ Bottom line:

For TRS, SURS, and SERS, FY2021 was one of the best investment years on record, but not uniquely the best—similar peaks occurred during the mid-1980s and mid-1990s bull markets.

Okay, got that boring stuff out of the way. What next?

.

.

.

Unexpected Mortality

.

Here is where I would usually be going back to all the annual reports and begin showing you the members removed from rolls tables and any death benefit/refund information. But I have looked at all that stuff for these three pensions and it is underwhelming, according to what they have published. Everything looks pretty hunky dory, almost as if there wasn’t even a pandemic in Illinois.

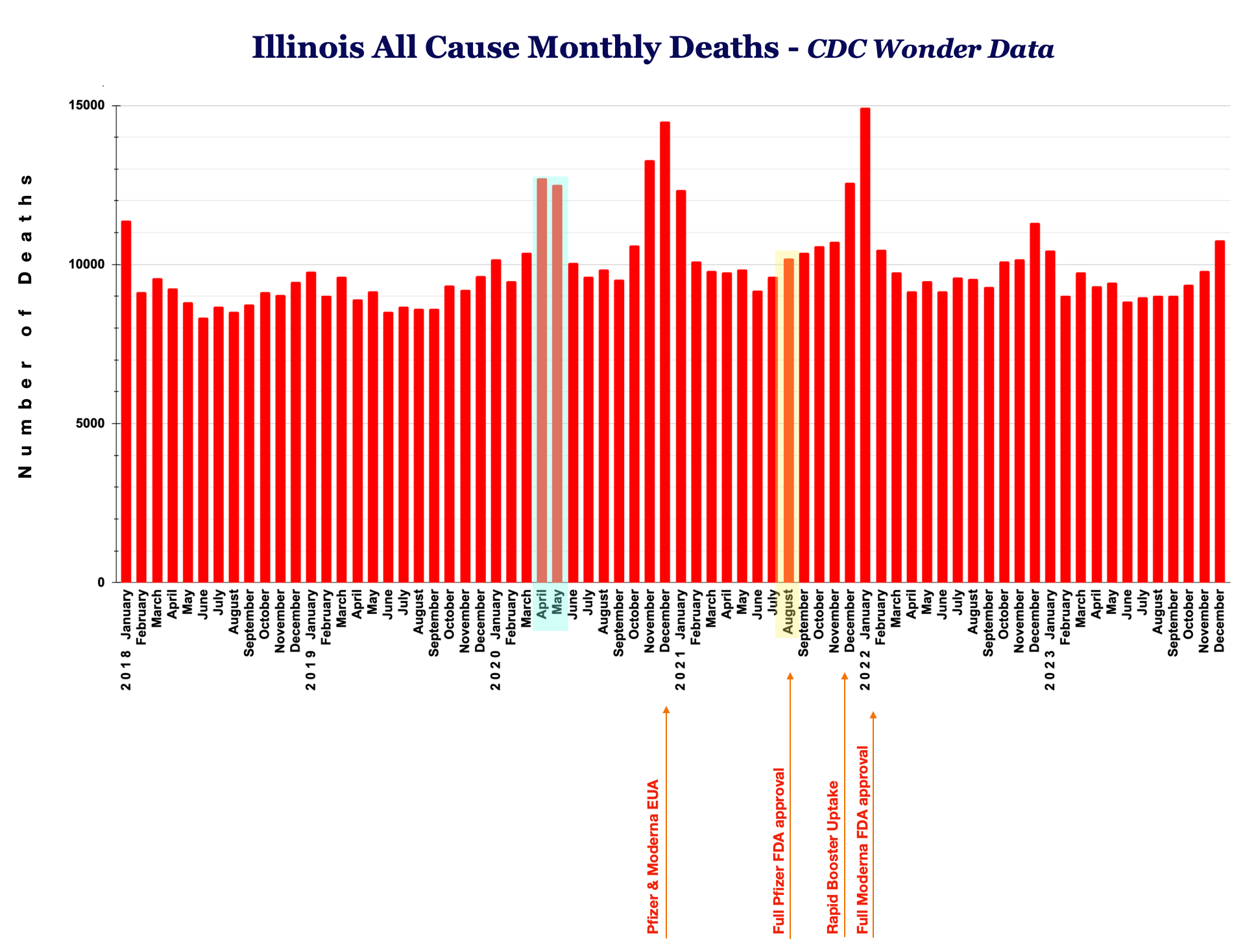

Hmm … that’s not what I see on that CDC graph right above.

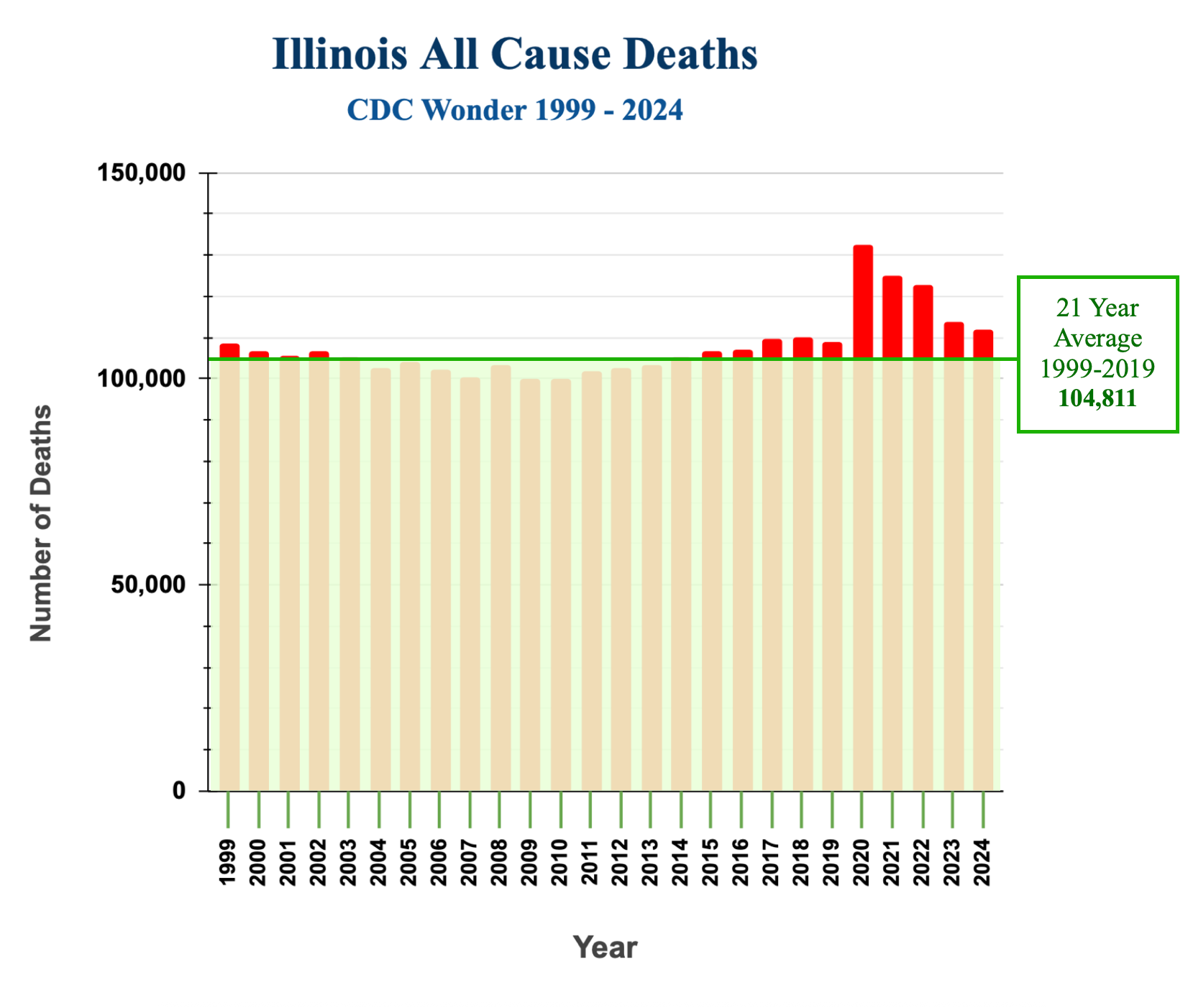

.

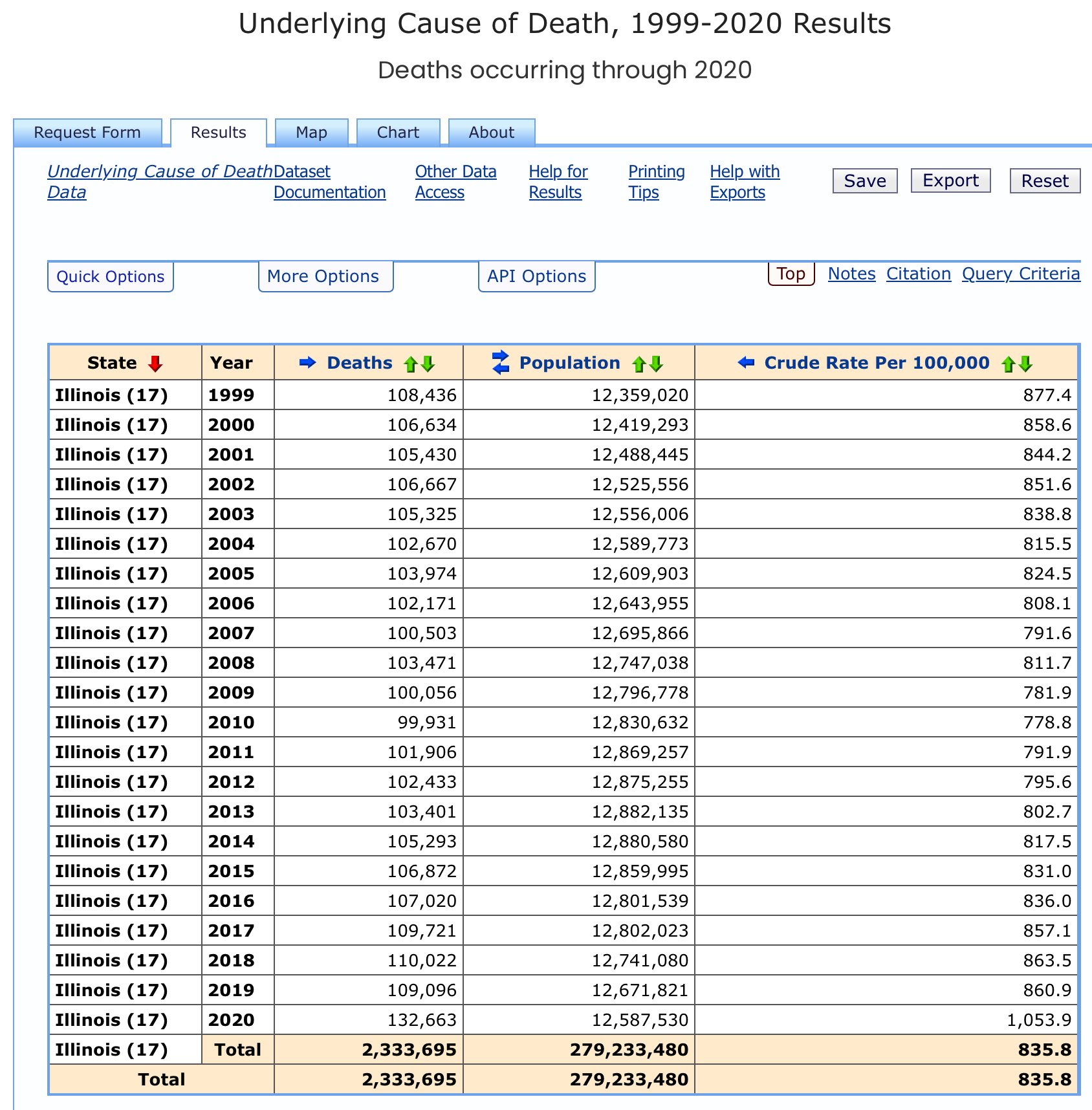

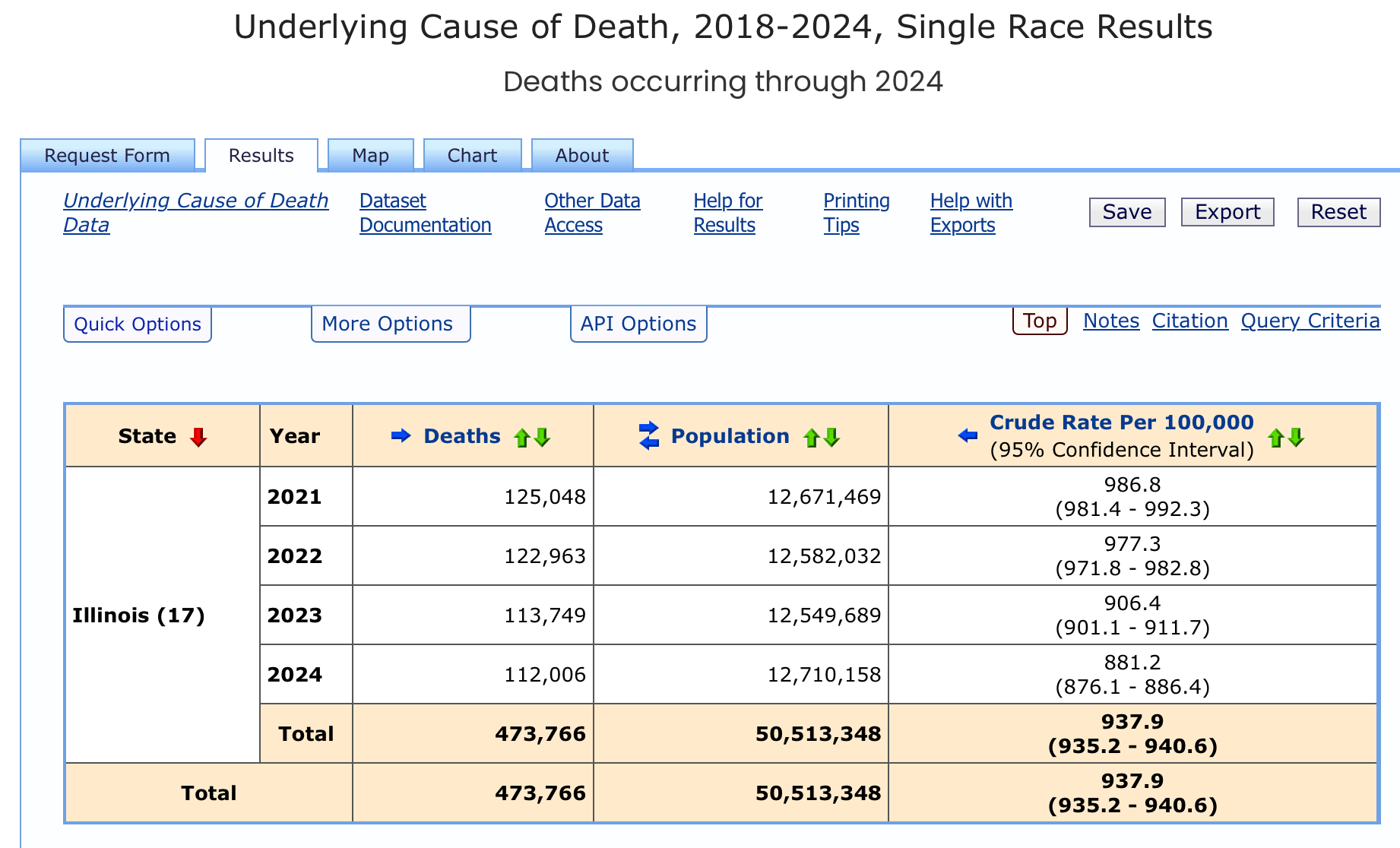

I think what I will do now is go back to the CDC Wonder database and convert that monthly graph up there to a yearly one. I will expand the year range to go all the way back to 1999 so we get a really good baseline average, well before the “covid” erupts. Then we will see if anything jumps out, but I bet my perceptive readers already know what we will find.

.

*If you are fairly new to this dusty storage room on Substack where I have my digital filing cabinet, then you may need a little explanation about what CDC Wonder is and how to use it. Please go back to this old post of mine to get that stuff explained.

.

Here are the raw numbers from CDC Wonder that the above graph was made from:

.

.

.

So at the risk of sounding like a broken record, when do we see the evidence of how awesome these “vaccines” were supposed to be? Why do the years after when those experimental medical interventions were administered have such high mortality above the baseline?

2020 … no vaccines

2021 and after … with vaccines

.

It really is that simple folks.

.

Did they work?

.

That depends on what “working” means …

I actually misspoke a minute ago when I said that 2020 had no “vaccines” - Pfizer got the Emergency Use Authorization on December 11, 2020 - and Moderna followed suit one week later on December 18th. Is it just a coincidence that we see that giant spike in mortality in that same month? And if you compare the spikes, it is even larger than the Illinois Ghost Bomb itself from April/May.

Was it truly just a more virulent strain of “covid” that had lain dormant through the summer waiting to erupt at the same moment in time as when the miracle drug was offered?

You be the judge.

.

.

.

Oh bother. I thought I was just going to go do some screenshots of those boring tables in the annual reports, dump them in the supplemental and call this one done. My mind is turning to mush again.

But …

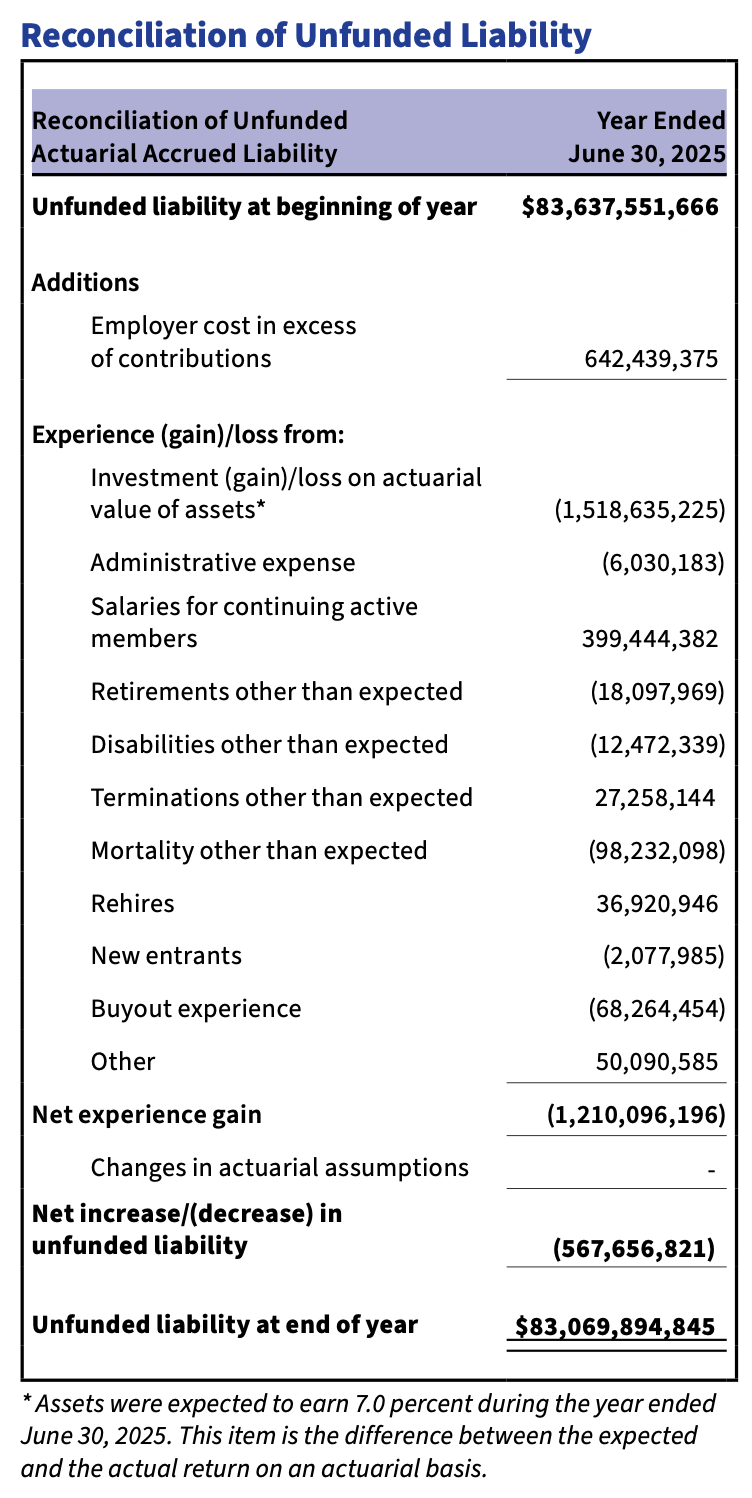

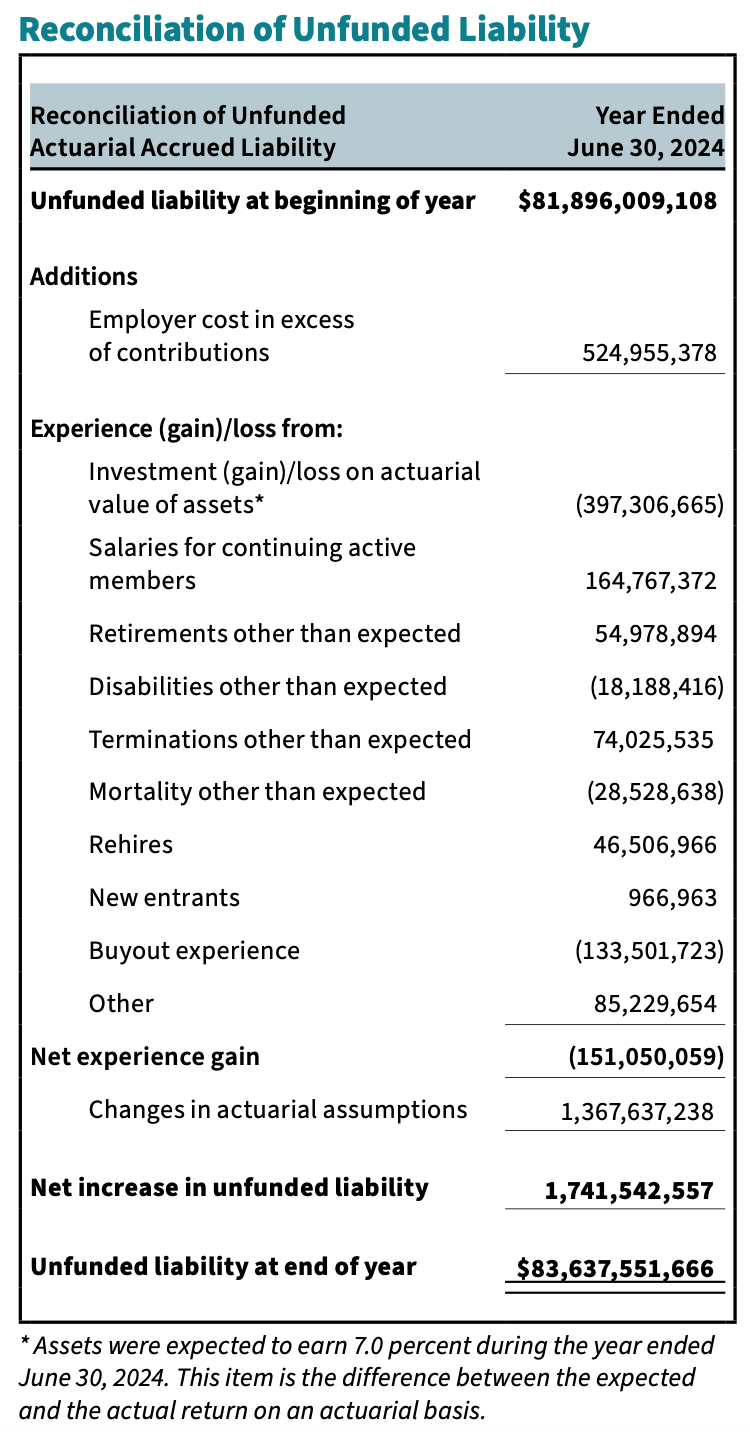

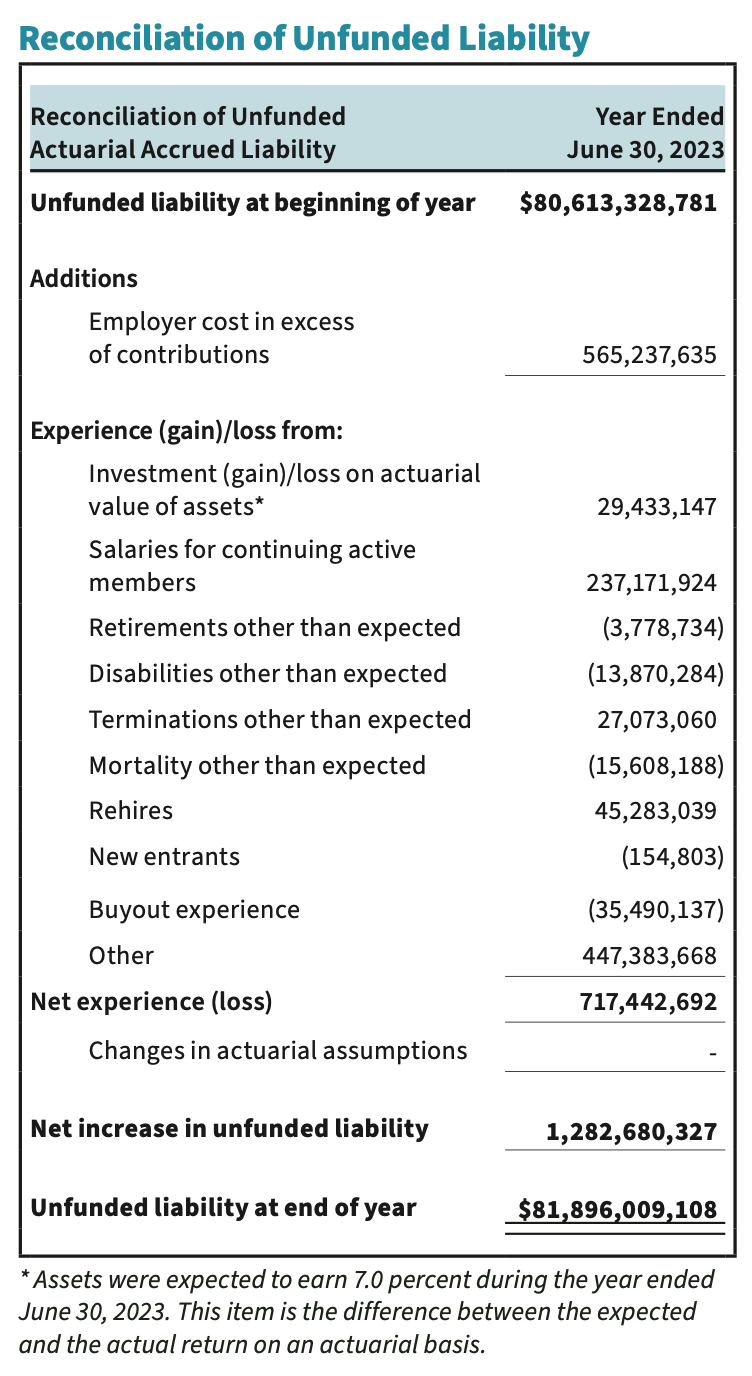

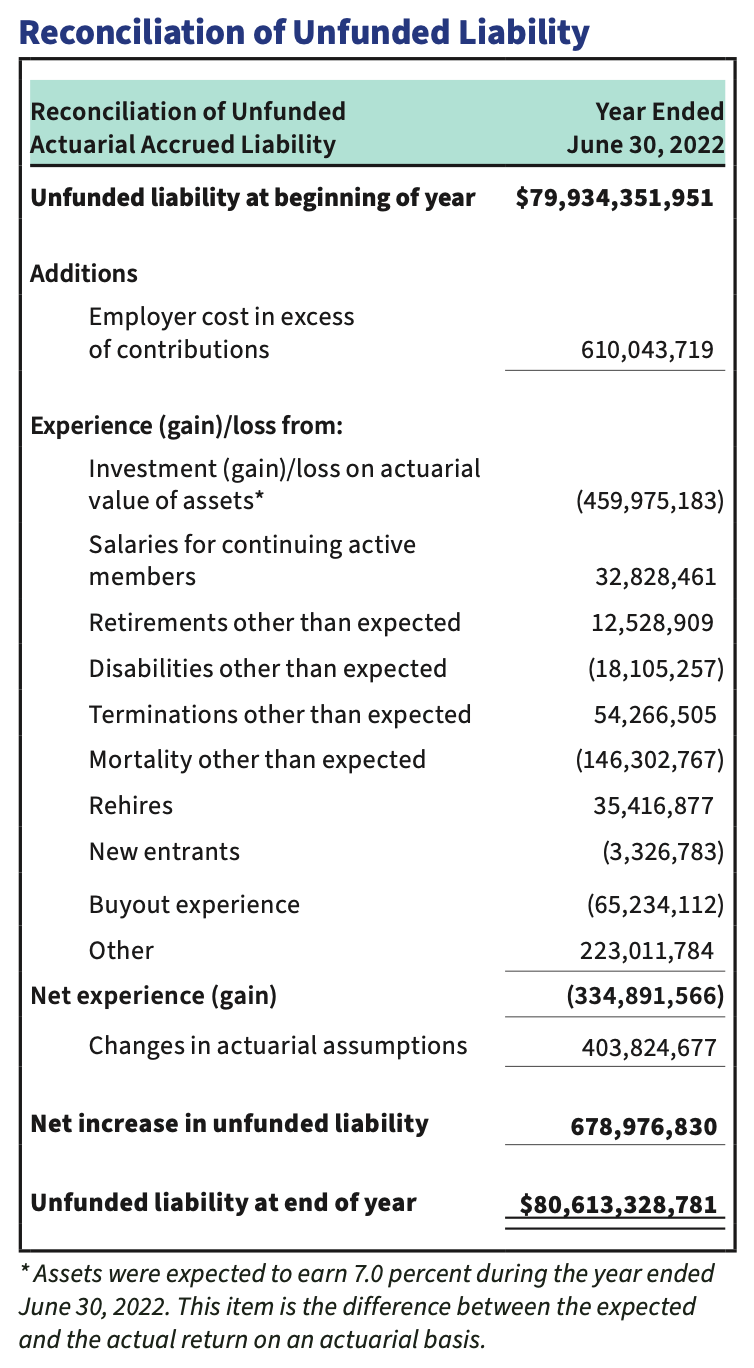

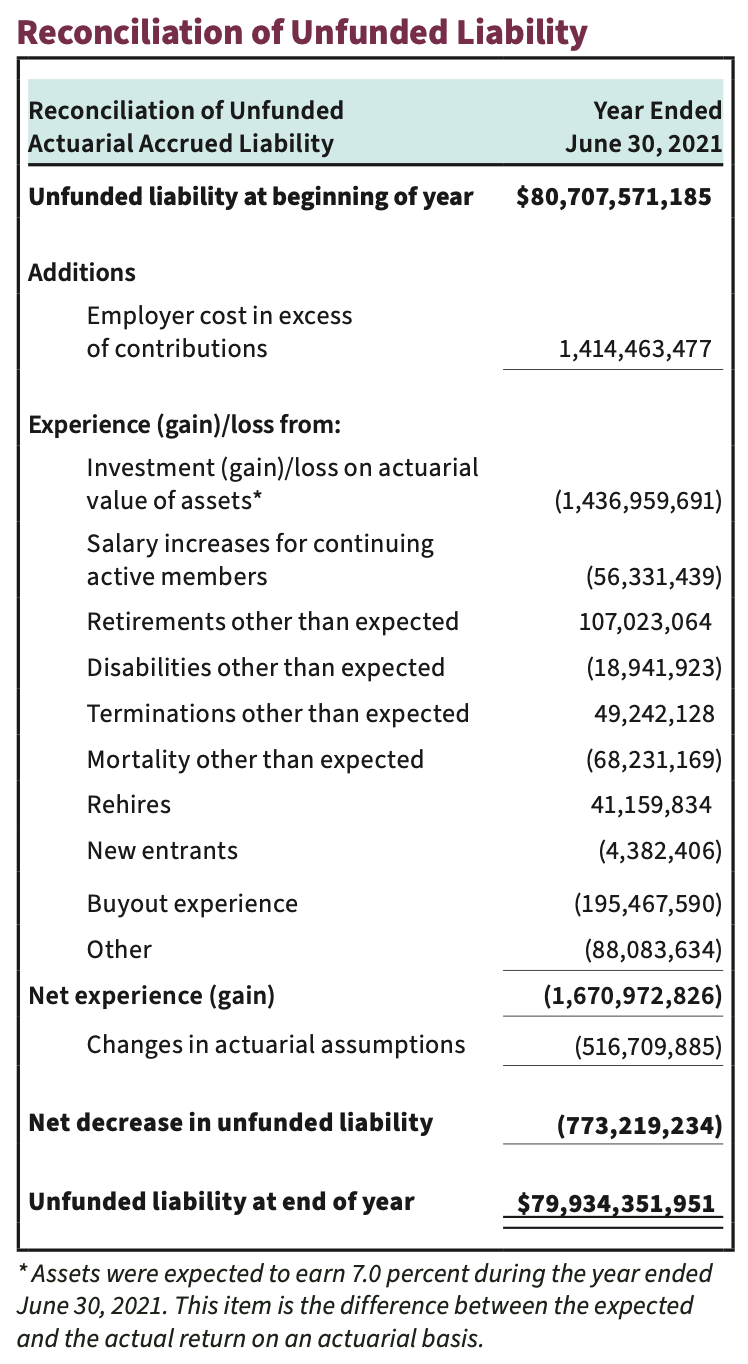

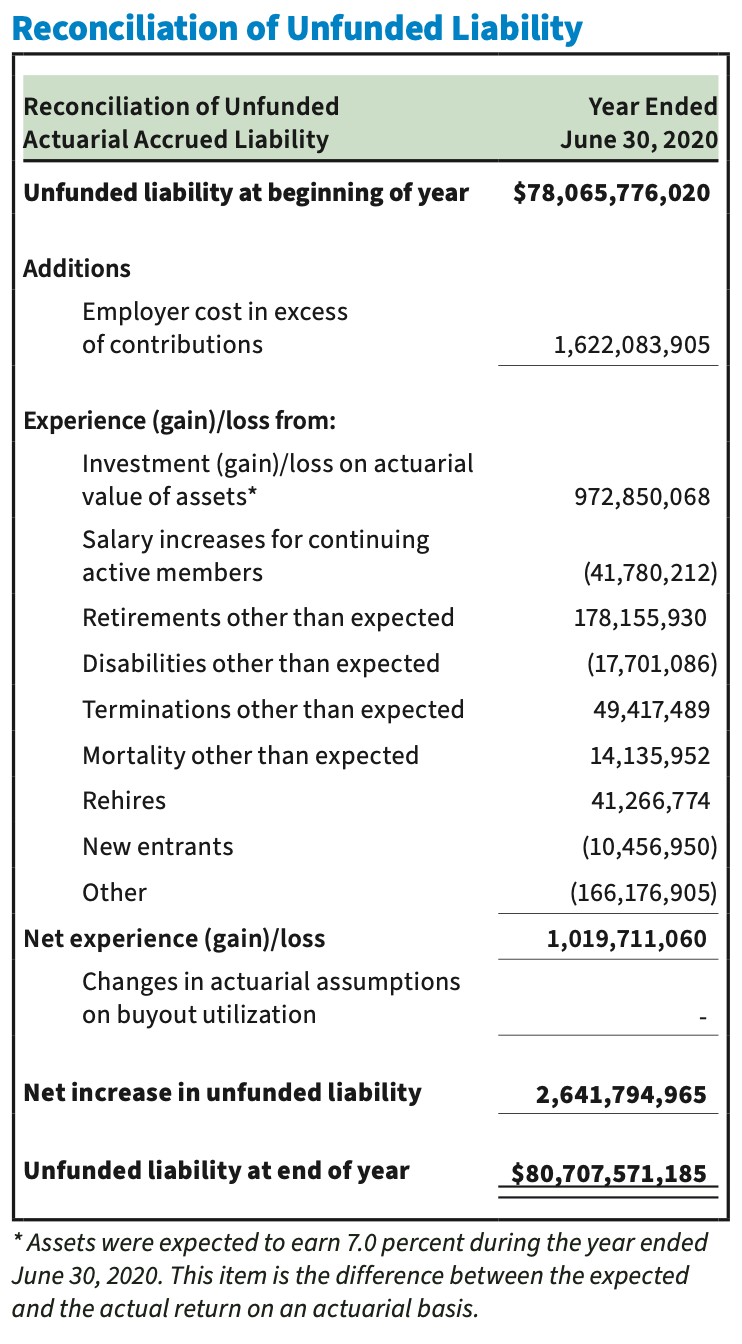

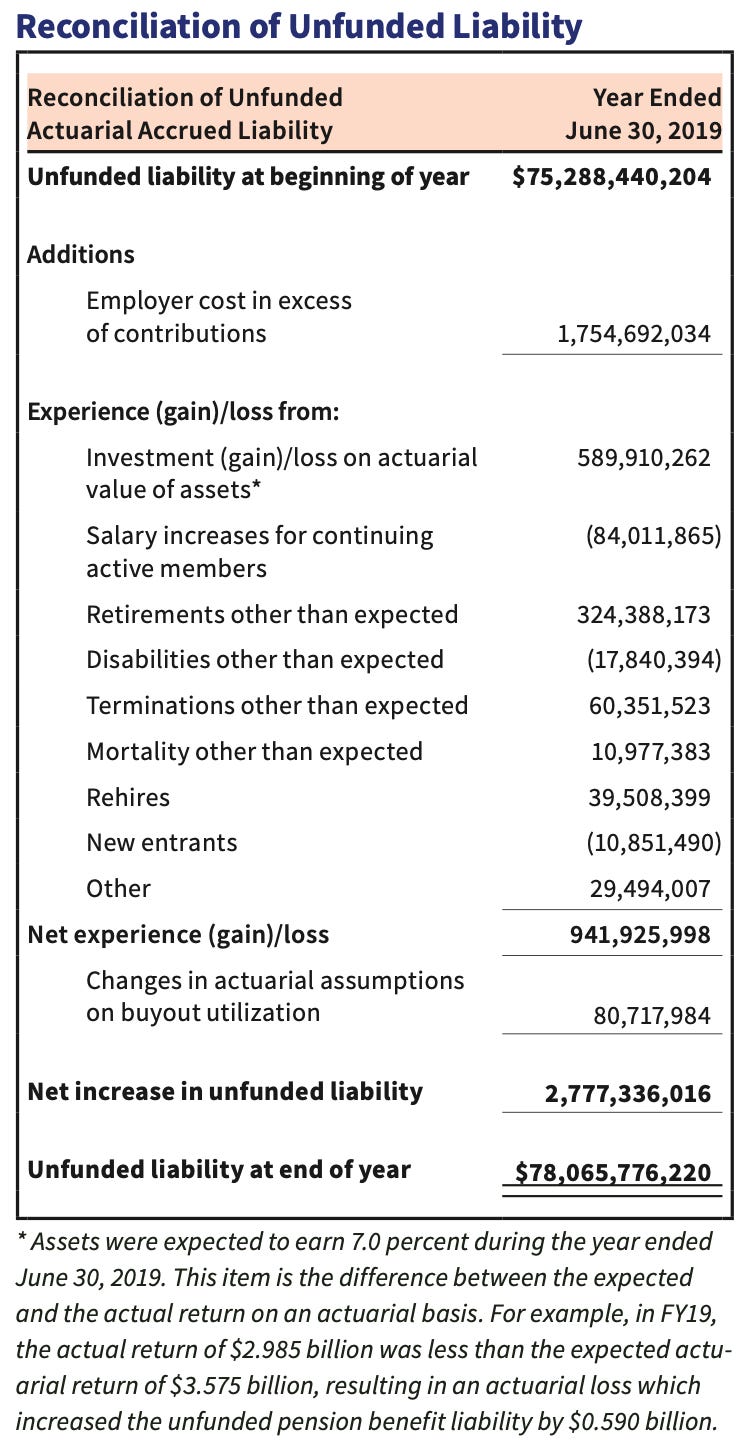

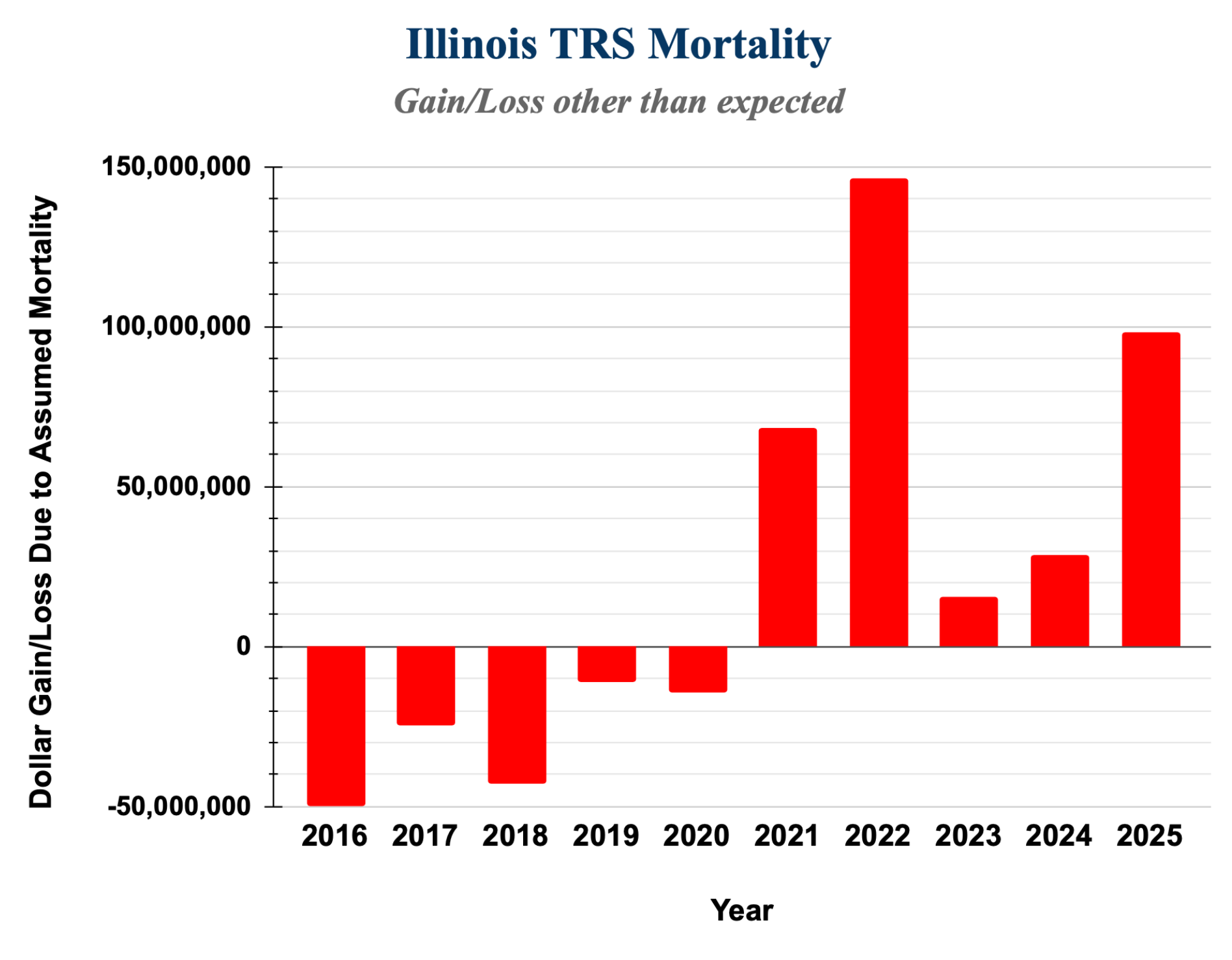

… as I started doing that, I just had to pay attention to this damn table in the TRS report:

page 91

.

Yeah, that horrible line that says “Mortality other than expected” is the problem. And if that number is in a parentheses on this table it is treated as a gain:

.

So what does that mean? I still get confused when looking at these and I had to give myself a refresher … went and asked Chat (I’ll give you the whole answer in the supplemental):

✅ So in your table, a gain in “mortality other than expected” means mortality was higher than expected (more deaths).

.

Yeah, that is what I thought.

So here we are in 2025 and the actuaries were way off in their mortality guess to the tune of 98 million dollars!

.

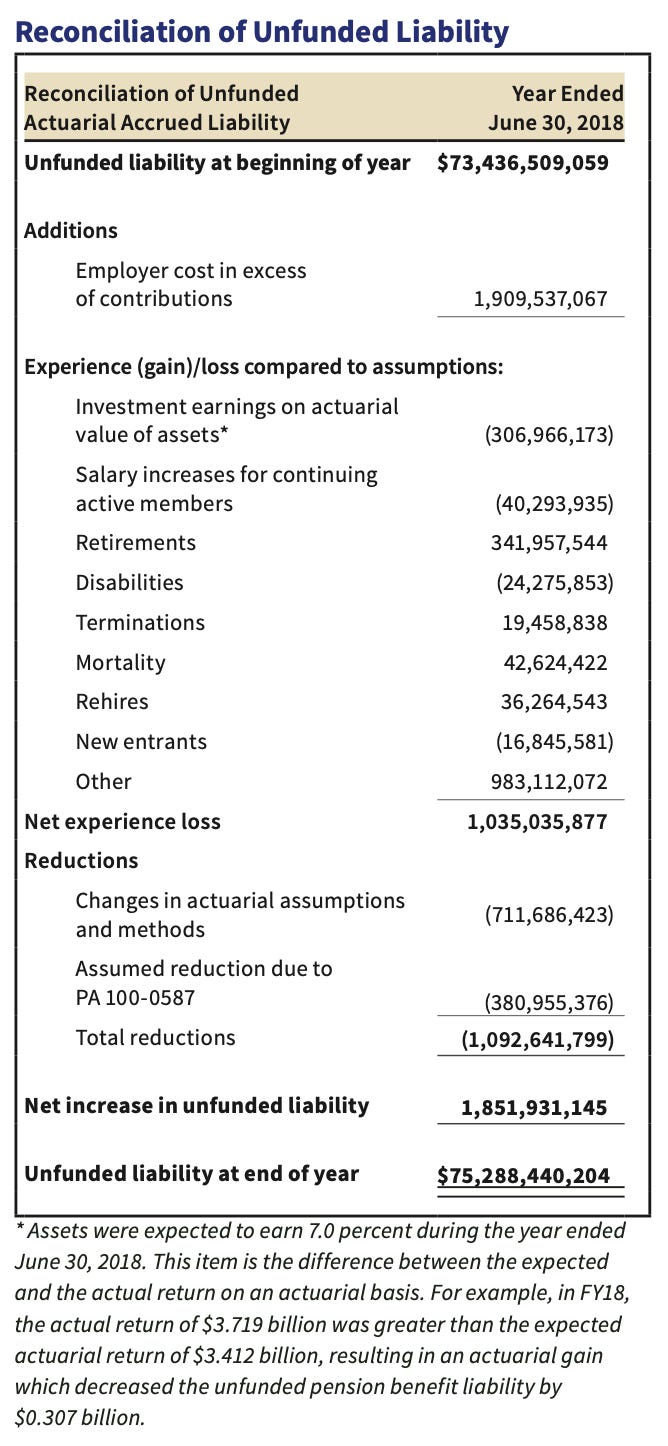

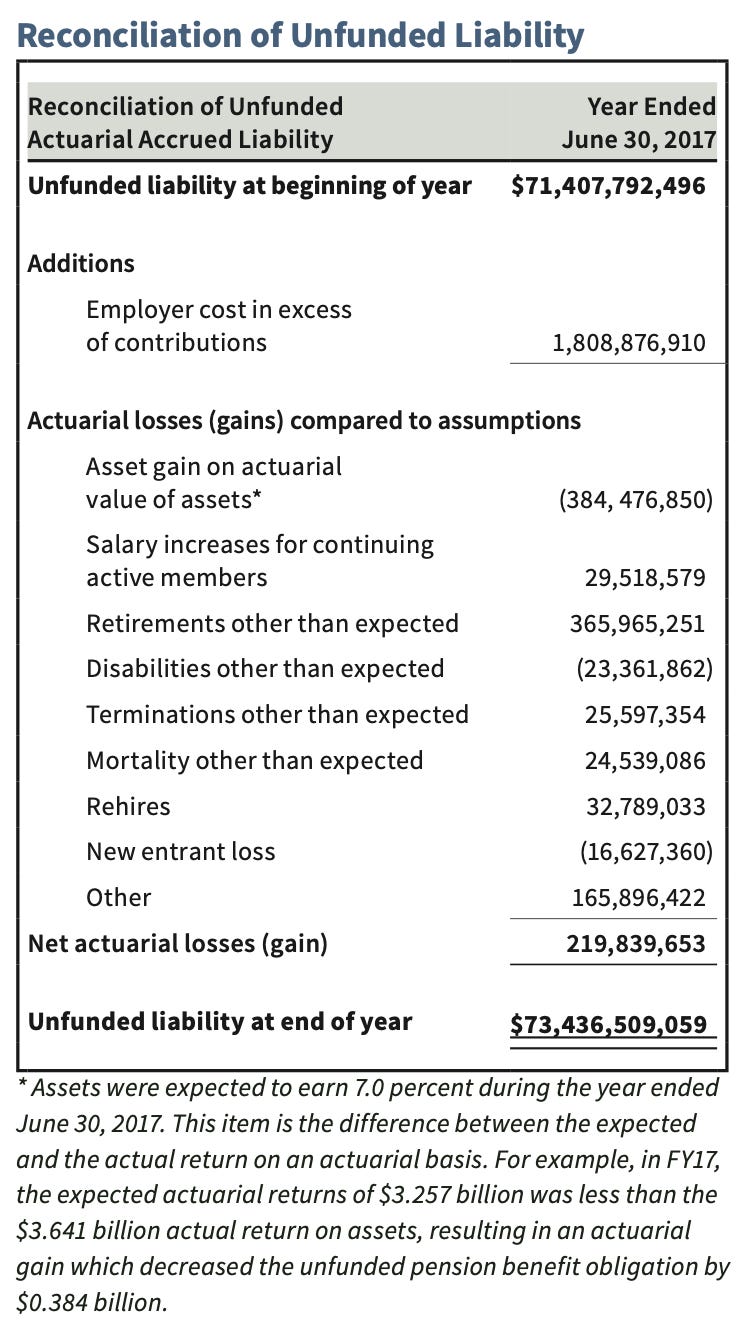

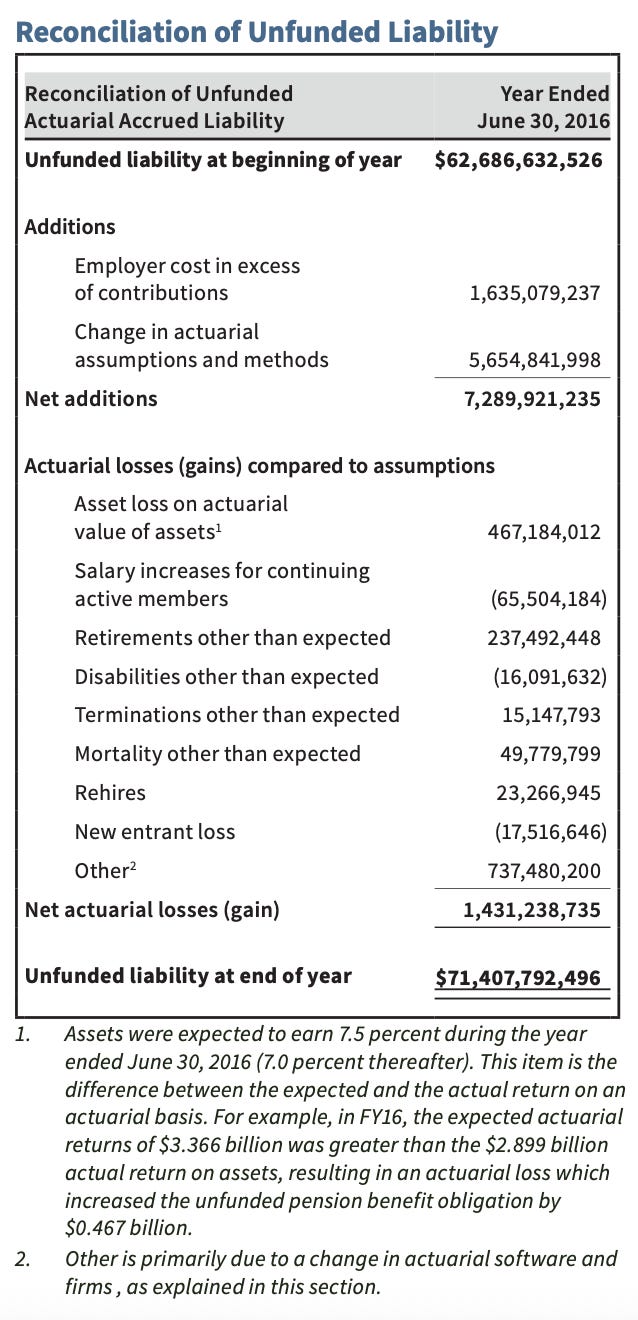

Now I am going to have to go look at the older reports.

Dammit.

.

.

.

.

.

.

.

.

.

.

.

.

Okay let me help visualize all that for you.

.

.

This is showing us that way more people started dying in 2021 than they expected.

.

Not in 2020 … apparently they expected better what happened in 2020.

.

Everything hanging down under that 0 line from 2016 to 2020 means that less people died than they expected.

Everything above that 0 line from 2021 to 2025 means more people died than they expected.

2021 was bad, but just look at 2022 and 2025.

Not good.

.

.

.

Folks, I could hunker down and give you all the gory details from each one of those reports. But I think this one is getting too long at this point. Maybe I will do a follow up later.

.

That’s what I got.

Supplemental

.

ChatGPT on rate of returns:

.

My Question: “were these historically the best or one of the best returns for each?”

.

Yes — FY2021 was one of the best investment years in the history of all three systems, though whether it was the single best varies slightly by system.

Below is the historical context based on their reported annual returns.

Teachers’ Retirement System of the State of Illinois (TRS)

FY2021 return: 25.5%

Historical context

This was among the highest returns in TRS history.

Comparable strong years include:

FY1986: ~26–27%

FY1995: ~26%

FY2014: ~19%

Most years historically fall in the –5% to +15% range, so 25%+ is extremely rare.

✅ Conclusion: FY2021 was one of the best years ever, but not definitively the highest.

State Universities Retirement System of Illinois (SURS)

FY2021 return: ≈23.8%

Historical context

This was one of the top returns in SURS history, especially since the fund diversified heavily into alternatives in the 2000s.

Comparable years:

FY2014: about 20%

FY1995: around 25%

✅ Conclusion: FY2021 ranks among the strongest years, though earlier 1990s equity booms produced similar or slightly higher returns.

State Employees’ Retirement System of Illinois (SERS)

FY2021 return: ≈24.9%

Historical context

This is near the top of the historical range for SERS.

Comparable high-return years:

FY1995: ~26%

FY1986: ~25%

FY2014: ~19%

✅ Conclusion: FY2021 was one of the strongest returns in decades, close to historic peaks.

Big Picture

Across all three funds:

Typical long-term assumed return: ~6.5–7%

Typical annual range: roughly –10% to +15%

FY2021: ~24–26%, which is 3–4× the assumed return

This happened because FY2021 followed:

the COVID-19 market crash in March 2020, and

a massive global equity rebound in 2020–2021.

✅ Bottom line:

For TRS, SURS, and SERS, FY2021 was one of the best investment years on record, but not uniquely the best—similar peaks occurred during the mid-1980s and mid-1990s bull markets.

.

.

.

ChatGPT on “mortality other than expected”:

.

My Question: “Reconciliation of Unfunded Liability table. This is in a pension report. If there is a gain in “mortality other than expected” does that mean there was more mortality than expected or less?”

.

In a pension “Reconciliation of Unfunded Liability” table, a gain means the plan’s liabilities turned out smaller than previously expected. The wording “mortality other than expected” refers to differences between the assumed mortality rates and the actual deaths that occurred.

Key interpretation

Gain from mortality → More participants died than expected (higher mortality).

Loss from mortality → Fewer participants died than expected (lower mortality / people lived longer).

Why this happens

Pension liabilities represent expected future benefit payments.

If more people die earlier than assumed, the plan pays fewer future benefits → liability decreases→ actuarial gain.

If people live longer than assumed, the plan pays benefits for more years → liability increases → actuarial loss.

Quick summary

Mortality experienceImpact on benefitsResult in tableHigher mortality than expected (more deaths)Fewer benefits paidGainLower mortality than expected (people live longer)More benefits paidLoss

✅ So in your table, a gain in “mortality other than expected” means mortality was higher than expected (more deaths).

.

.

.

.

*in case you have forgotten …

Pandemic Milestones:

January 20, 2020

-First covid case in the U.S.

December 11, 2020

-Pfizer Emergency Use Authorization

December 18, 2020

-Moderna Emergency Use Authorization

August 23, 2021

-Pfizer full FDA approval

December 2021 / January 2022

-CDC and FDA revise booster recommendations

-Rapid booster uptake

January 31, 2022

-Moderna full FDA approval

August 31, 2022

-FDA authorized Pfizer and Moderna’s new bivalent COVID booster vaccines

April 10, 2023

-Biden declares the end of the pandemic

.

.

.

Thank you for keeping at this.

I didn’t know about that early “covid” death in Illinois either.

I do wonder about those big states Texas and California, which rank near the bottom with Illinois in terms of pension liabilities ..