Another Big Bang

CONNECTICUT ... 2020 Early Spring Deaths, Astronomical Investment Gains in 2021 & Unexpected Mortality After the Vaccine Rollout

Some of you out there reading my stuff may be wondering if I am ever going to get to the end of my obsession with my little “Ghost Bomb” research. It does just seem to go on and on. I know! Believe me, it is starting to get a bit much even for me. But why can’t I move on to something else?

I think somewhere in my hidden layers of understanding, I have known that this subject may be the key to the whole thing. Like trying to formulate a picture of the universe … you eventually end up back at the Big Bang.

You know, that explosion that started it all.

Let me ask you a question. Do you honestly think that what we all went through the last five years would have happened if “covid” had not burst onto the scene in an overly dramatic fashion? The people falling over in the streets in China, the horrible stories coming out of Italy in the spring of 2020 … and of course, the shock and awe that was New York.

.

Without these things scaring the “beejeezus” out of you, would you have locked down, masked, social distanced and ultimately agreed to put an experimental drug into your body?

.

If your answer is no, which I hope most sane people would say, then can you see why the Ghost Bombs going off as they did in the spring of 2020 was the turning point in this country for all that came afterwards?

I hope so.

As I hinted at in the last installment of my Ghost Bomb Six series, there may actually be more locations that could expand that number. Today we will take it to seven.

.

.

.

First let’s have a refresher and just list all the Ghost Bombs again:

*Ghost bombs are highlighted in blue.

.

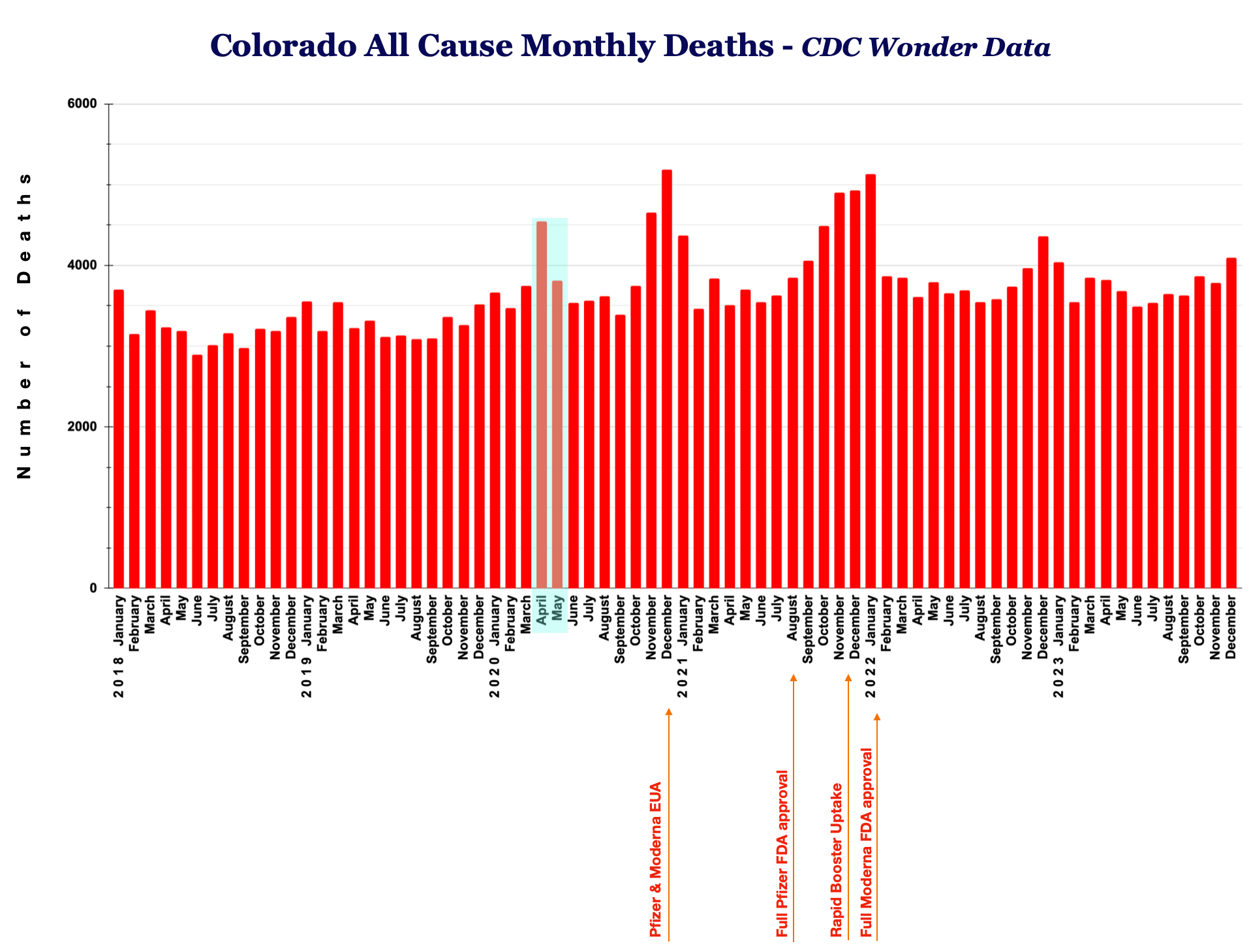

Colorado

Pension System Rank: 38

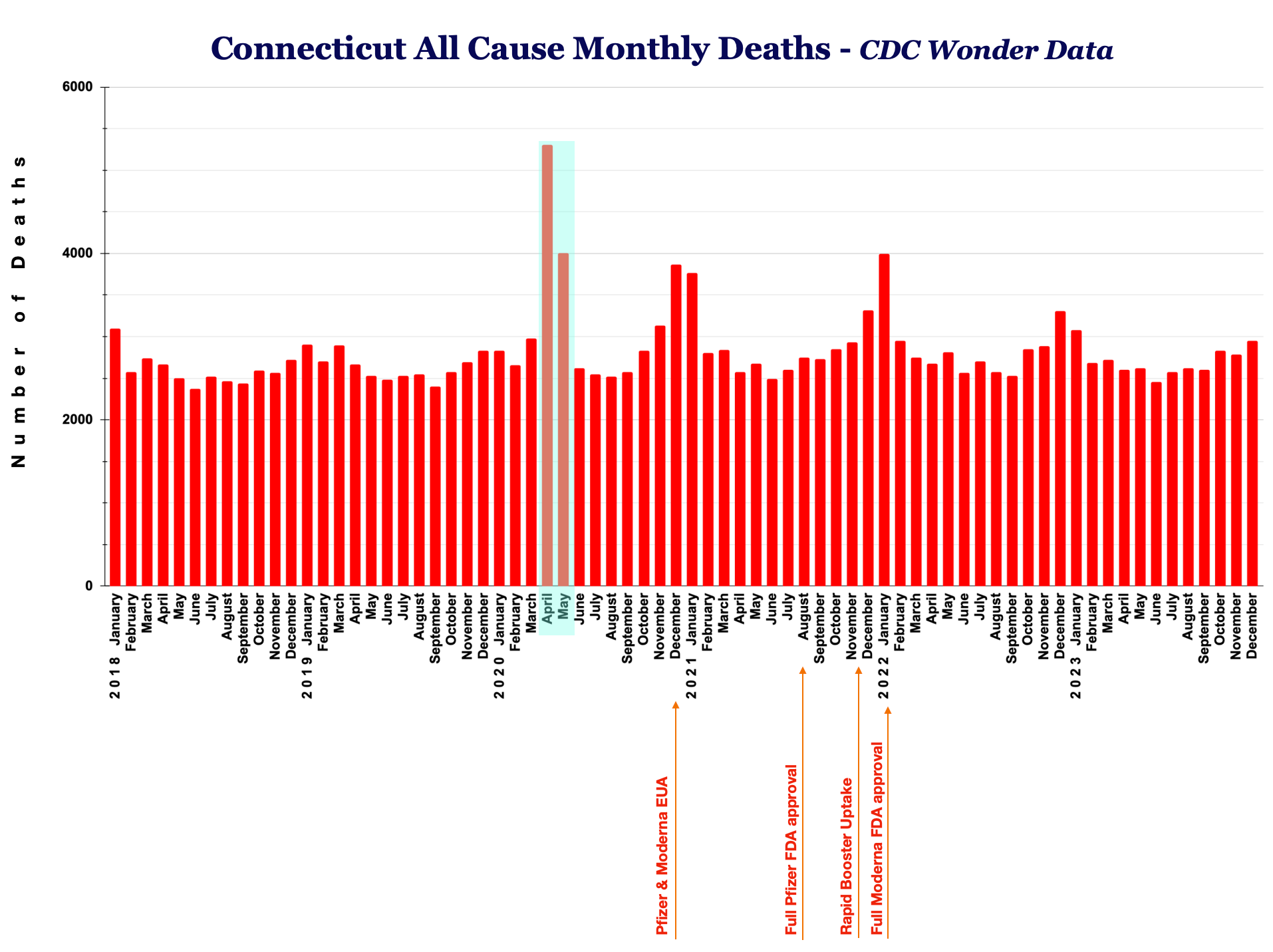

Connecticut

Pension System Rank: 35

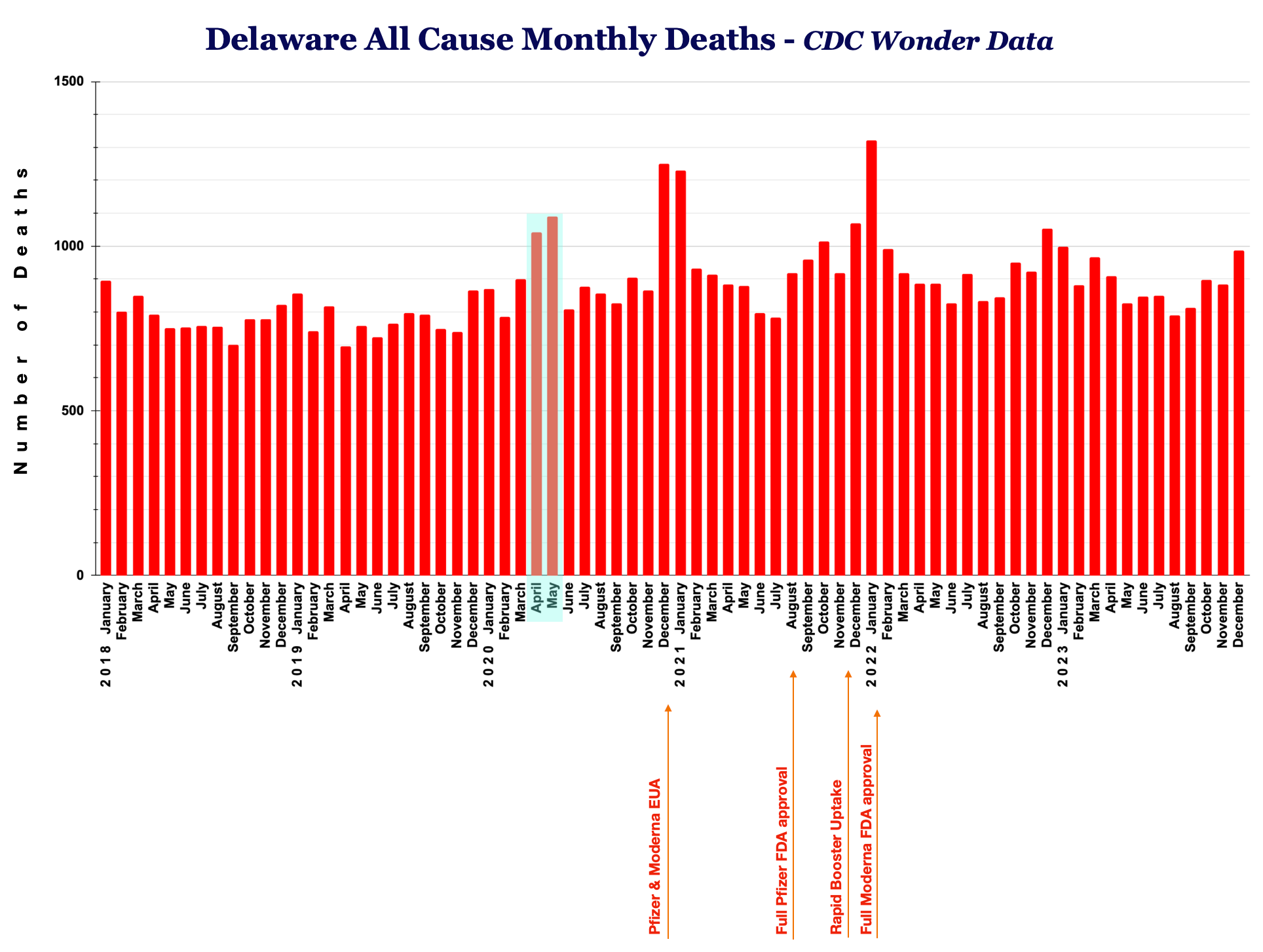

Delaware

Pension System Rank: 4

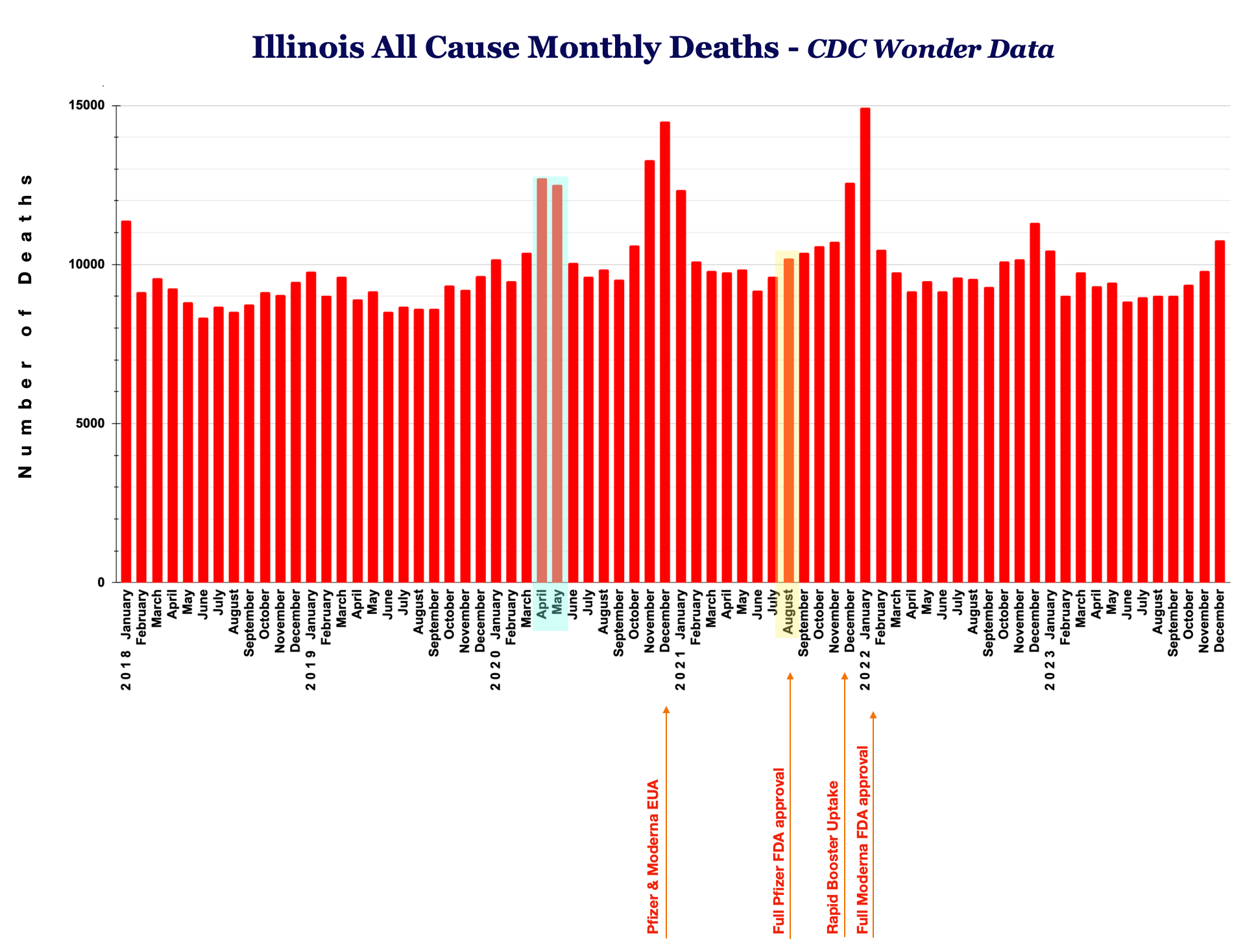

Illinois

Pension System Rank: 49

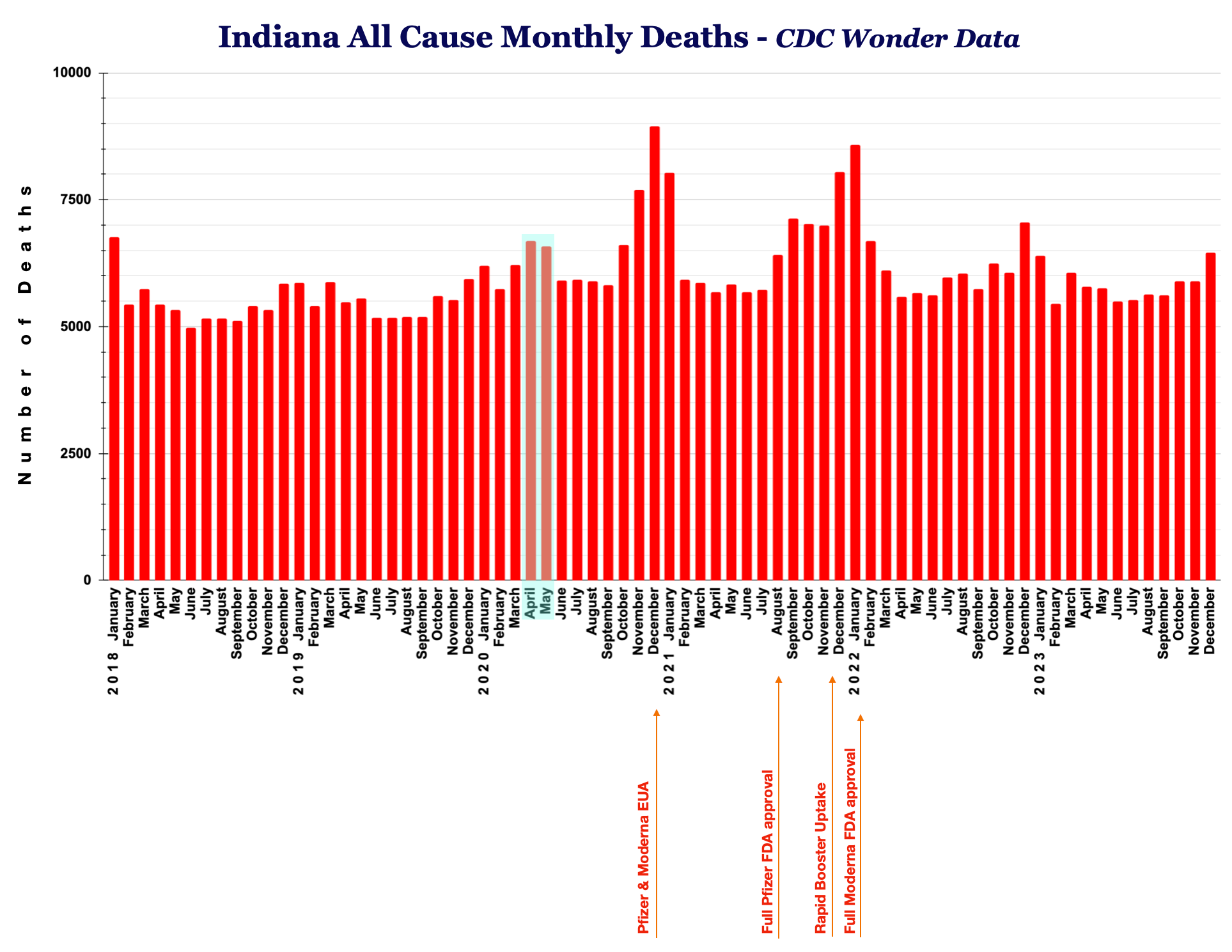

Indiana

(baby bomb)

Pension System Rank: 22

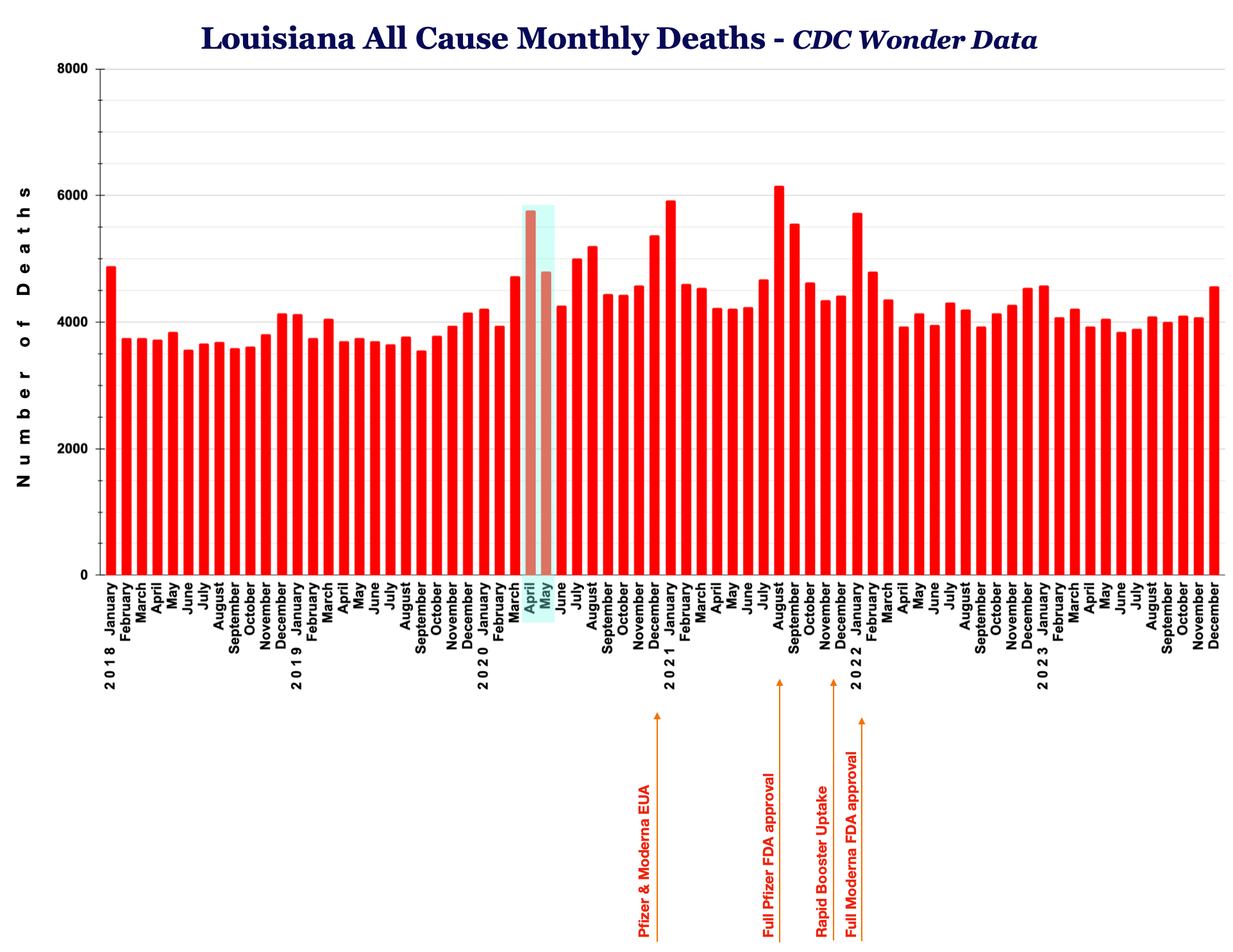

Louisiana

Pension System Rank: 29

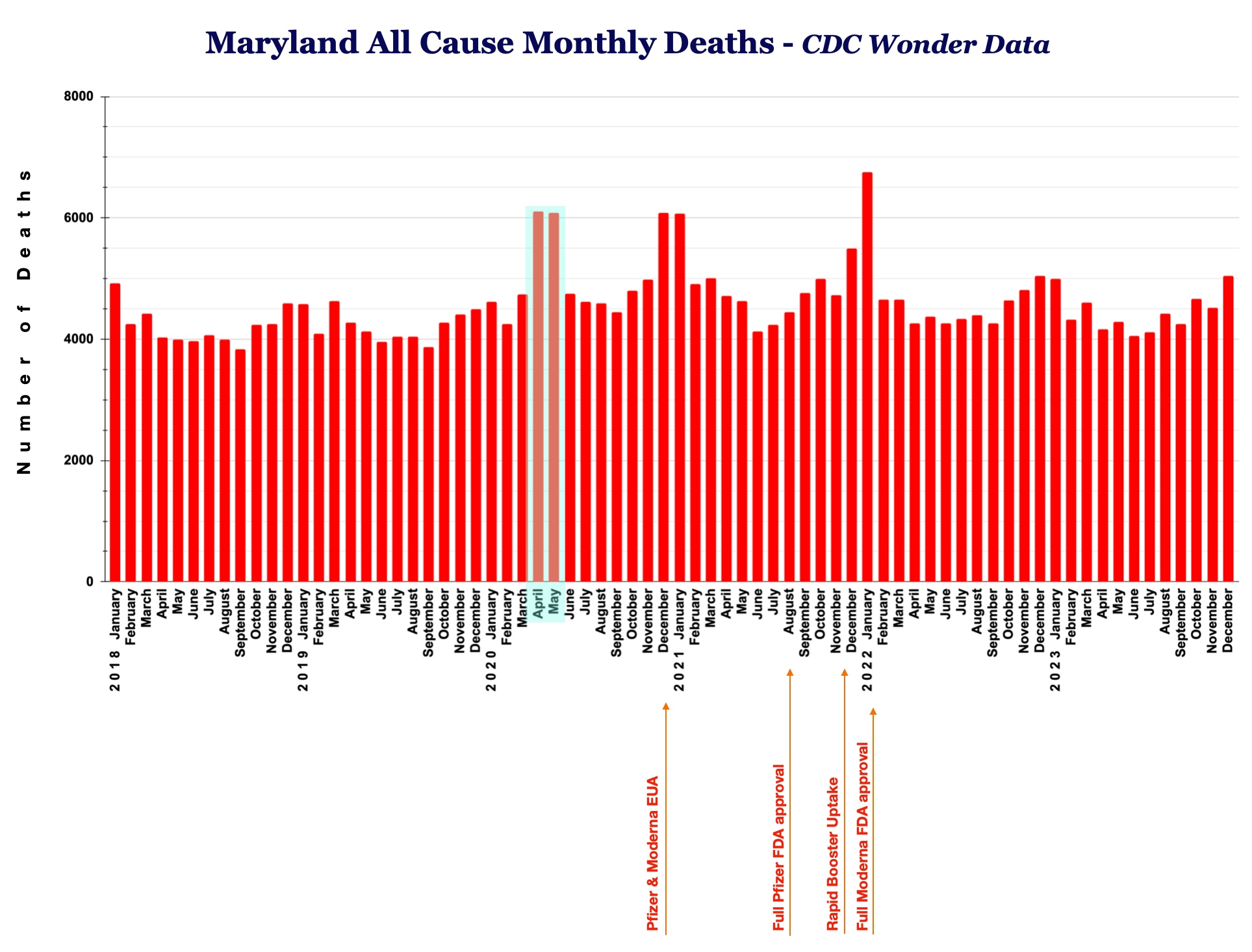

Maryland

Pension System Rank: 30

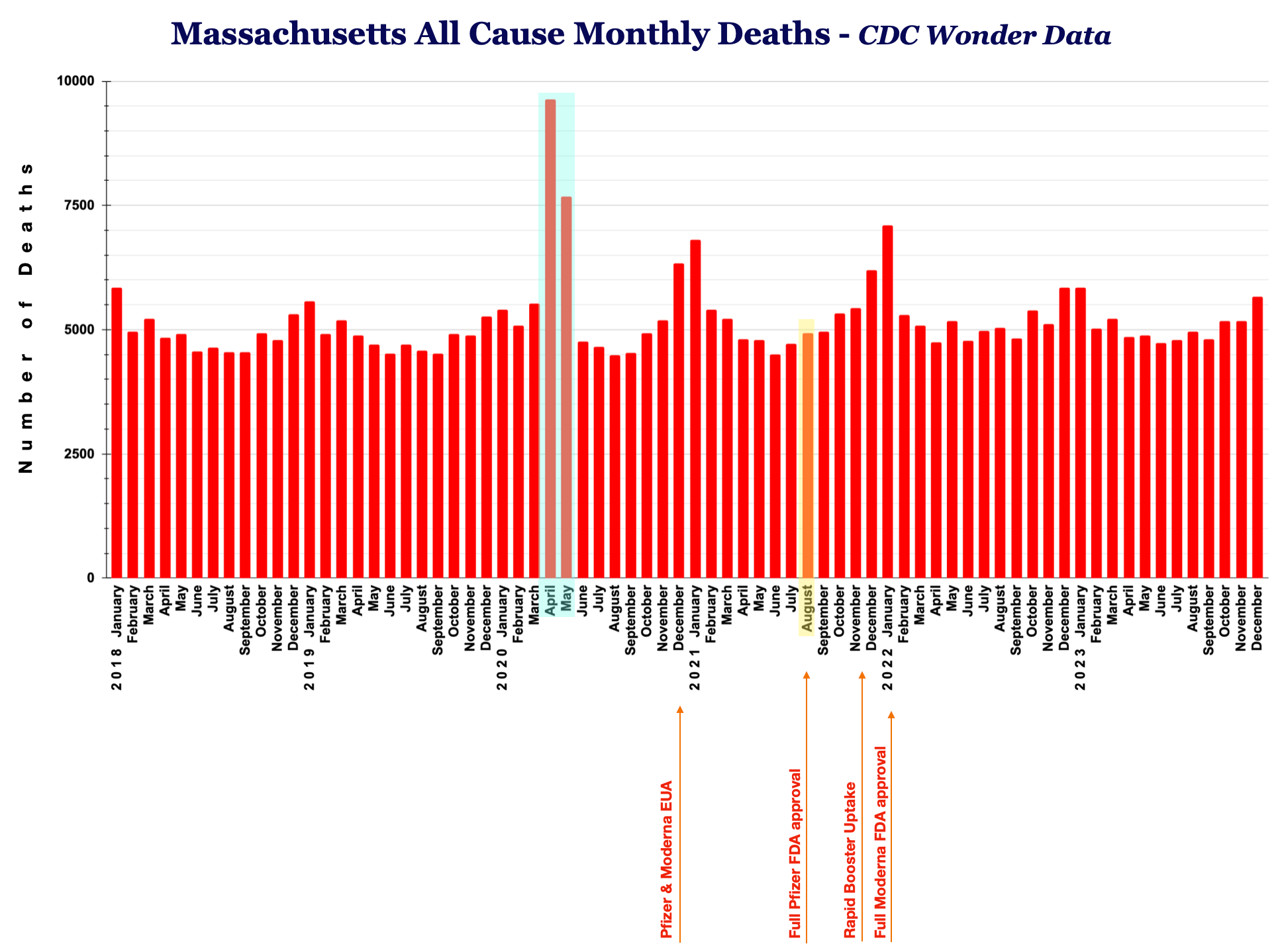

Massachusetts

Pension System Rank: 41

Michigan

Pension System Rank: 42

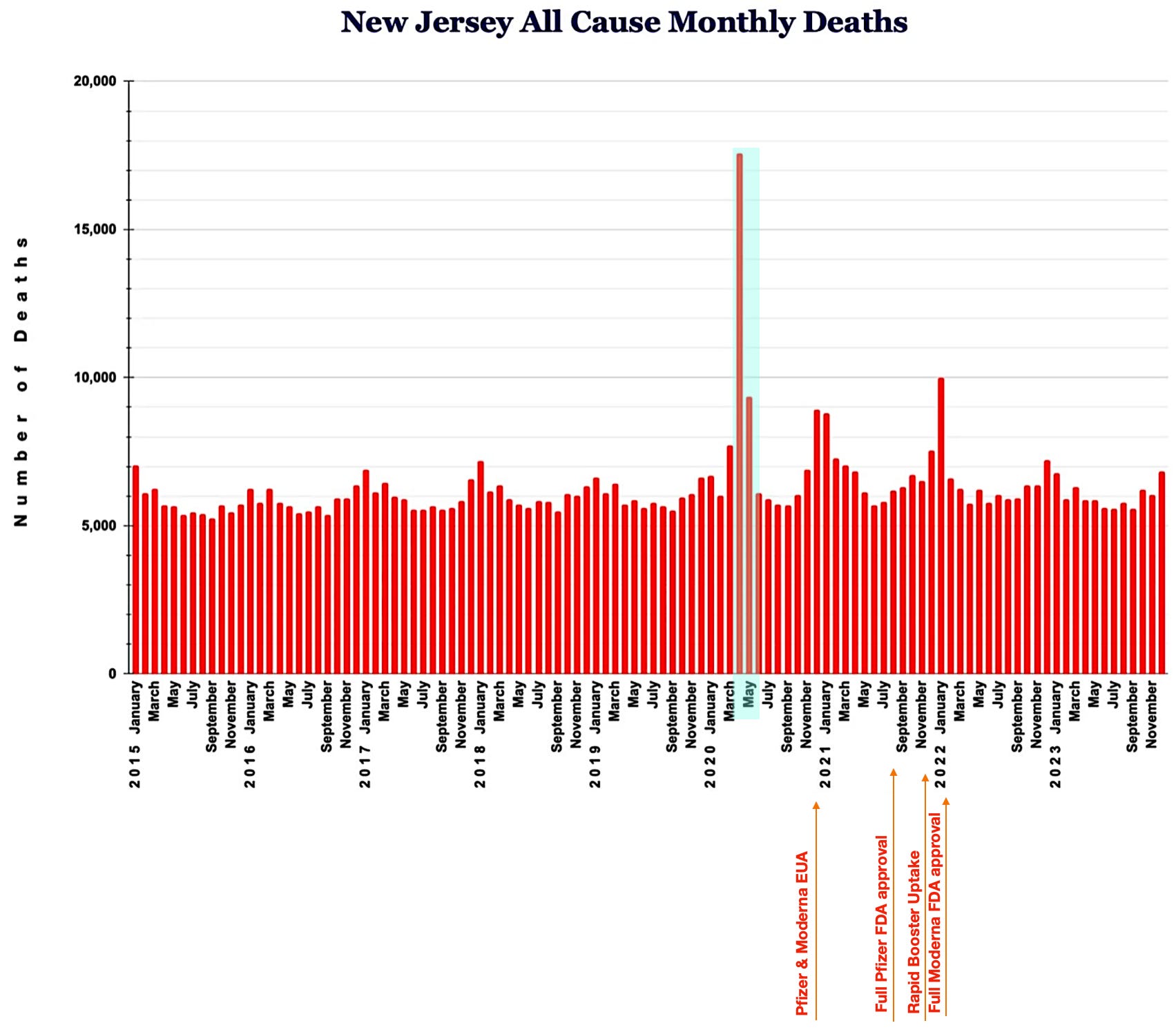

New Jersey

Pension System Rank: 44

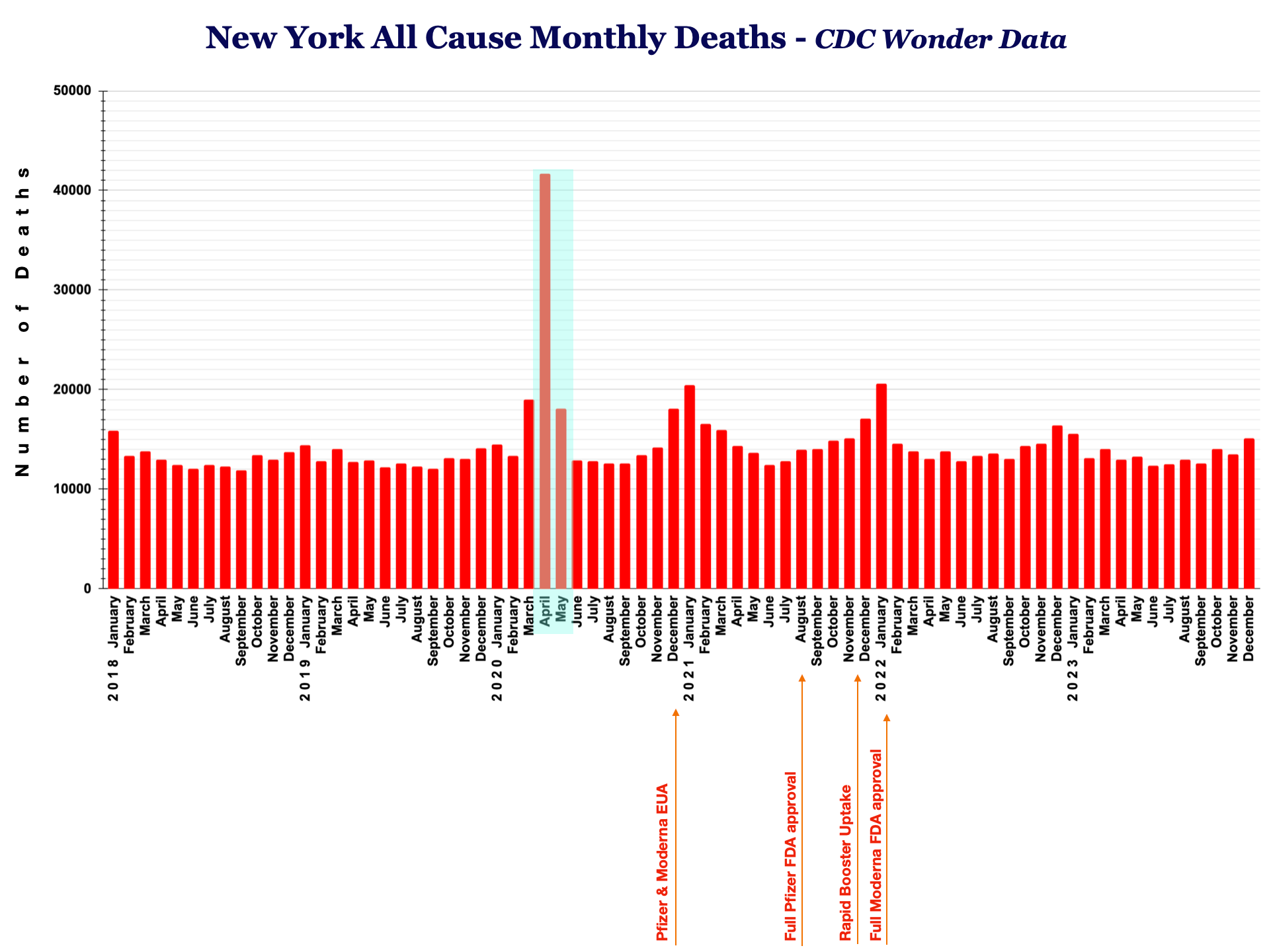

New York …

Pension System Rank: 46

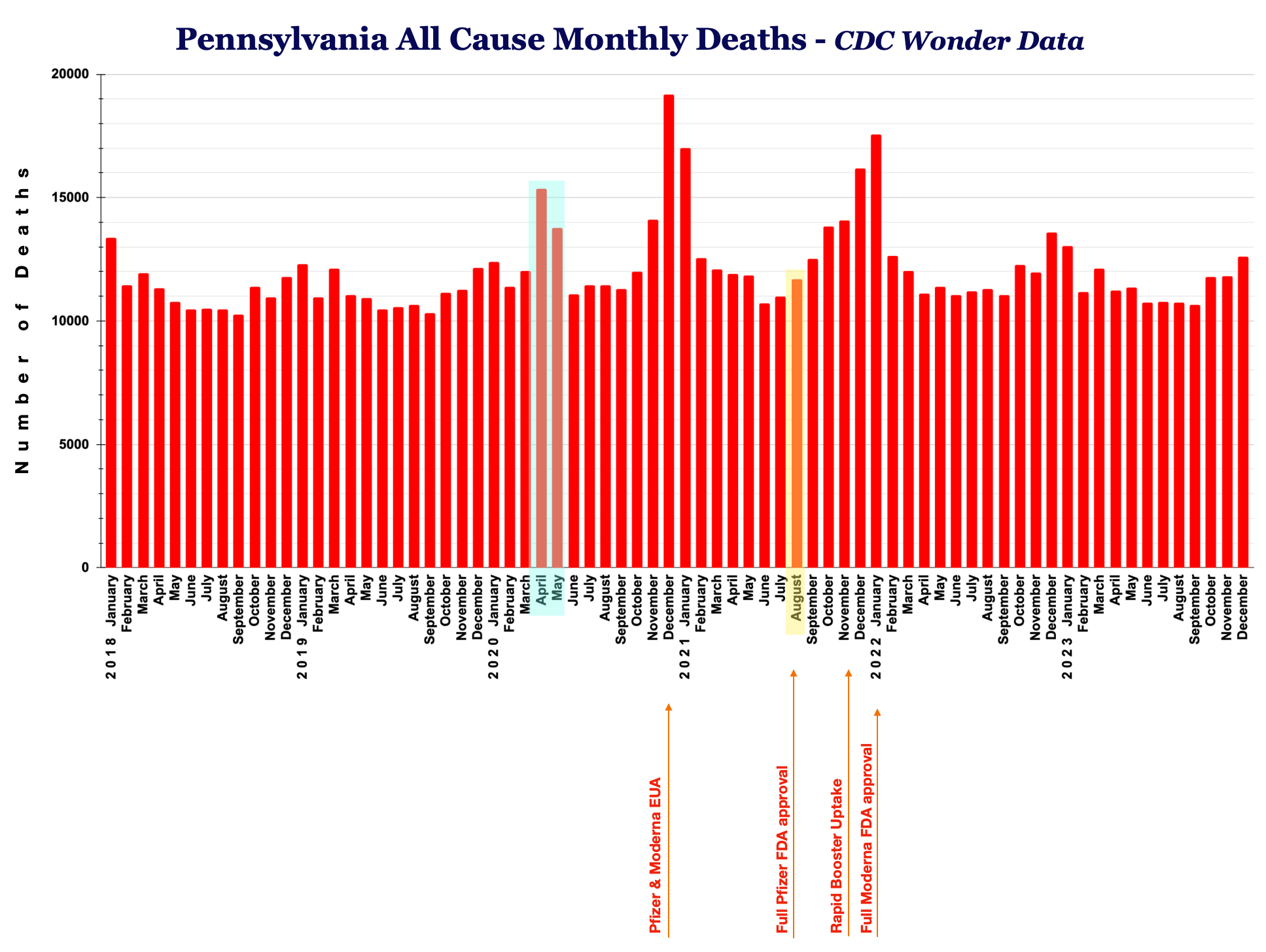

Pennsylvania

Pension System Rank: 45

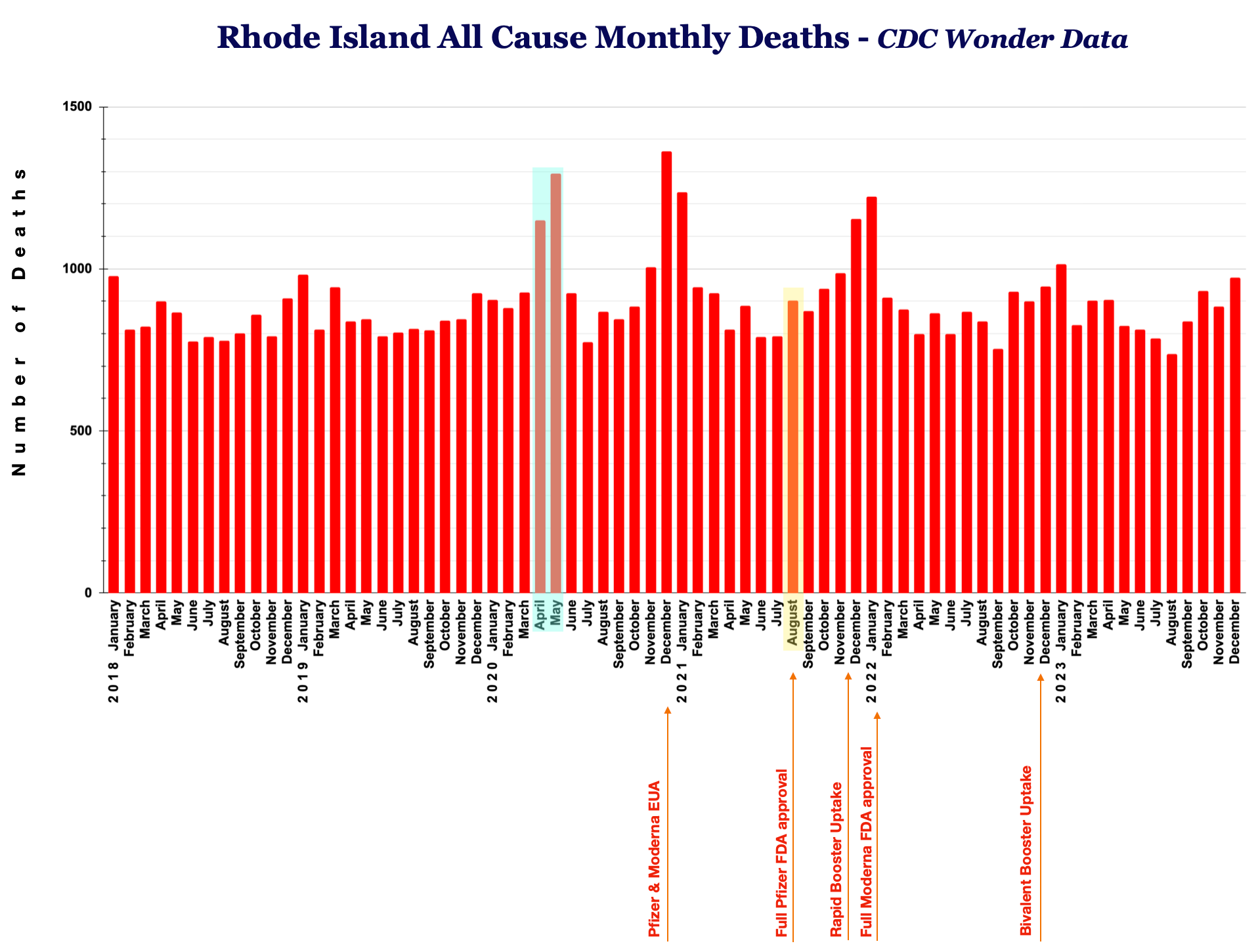

Rhode Island

Pension System Rank: 10

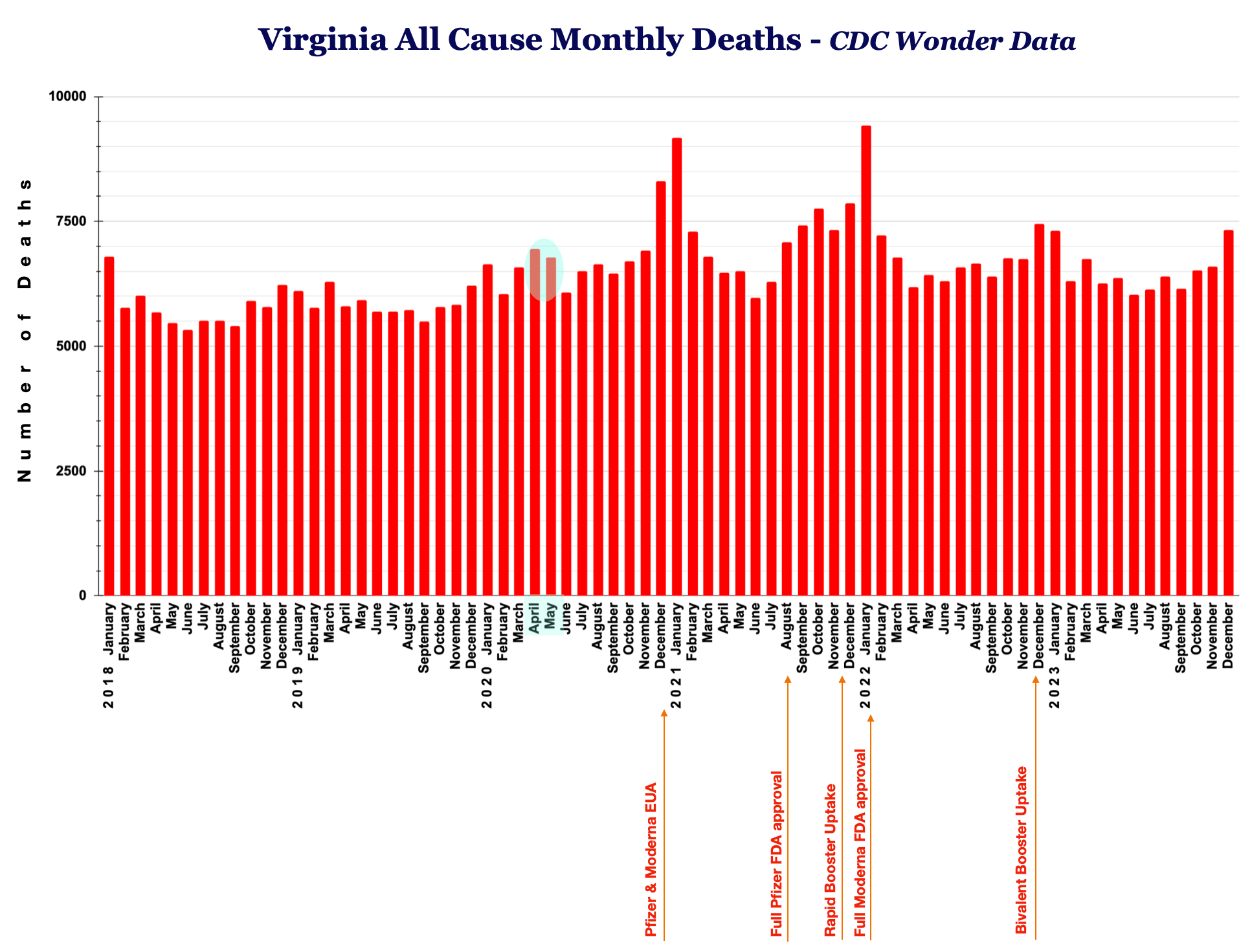

Virginia

(baby bomb)

Pension System Rank: 36

.

That is a 14 state list out of 50 that had a Ghost Bomb go off - two of those (Indiana and Virginia) had much smaller compared to the others.

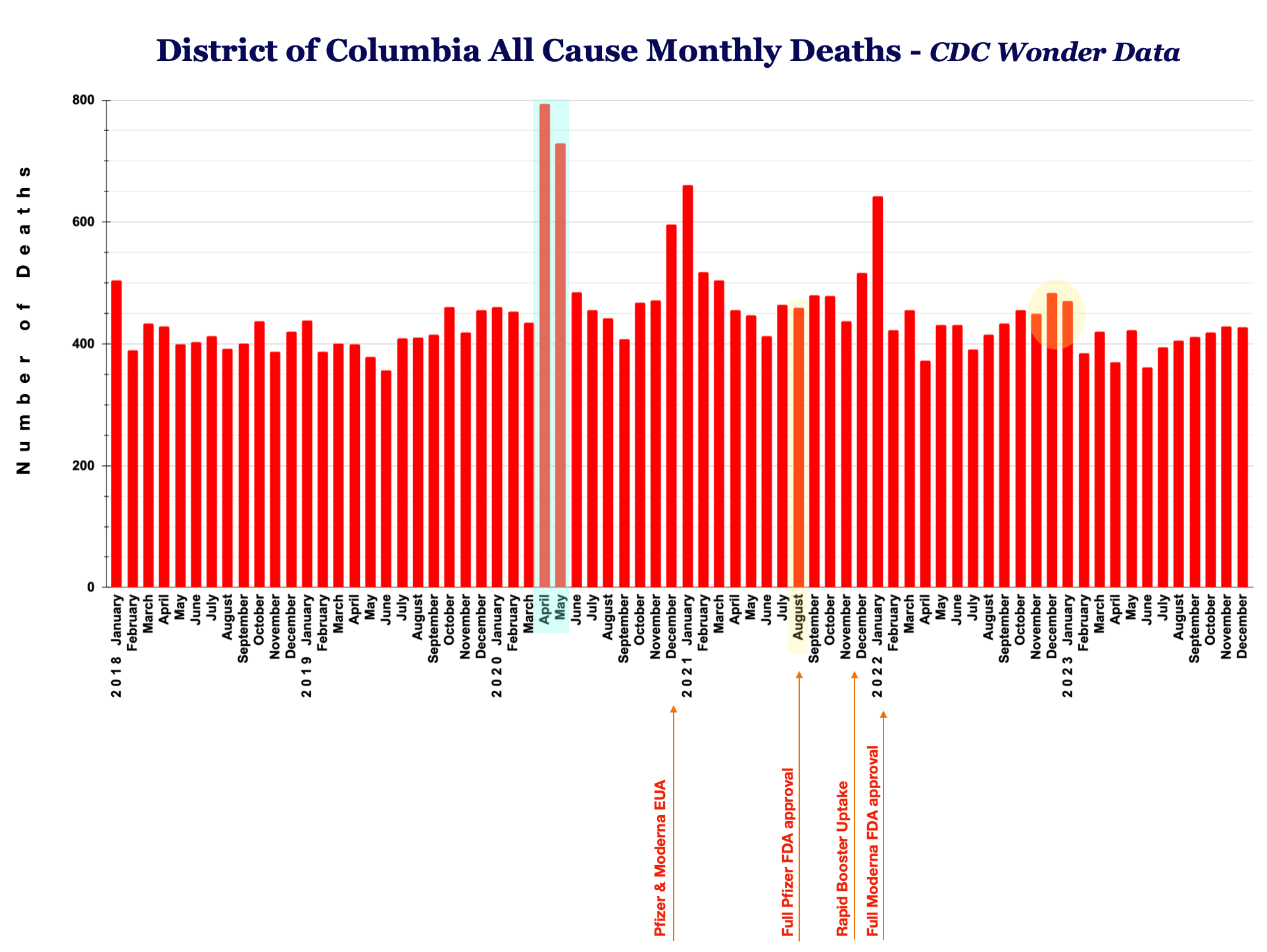

And just so you know … it is not on the pension ranking map, and so did not enter this list, but the District of Columbia had a pretty big Ghost Bomb.

.

District of Columbia

*(All of those pension system ranks come from an organization called ALEC - which, as we discussed in my last post, is not the only source for pension rankings. We will get to more on that a little further down in this post).

.

.

.

Okay, so there is the total list of these bombs that went off in April/May of 2020.

Personally, back in the spring of 2020, I was only truly aware of the one that went off in New York. And I bet that most people you talk to will be as unaware as me, or at least knew of only a few, not the entire list. But then again, I live on the west coast, where no Ghost Bombs went off at all.

.

What again is the Ghost Bomb Six and what do the pension ranks have to do with anything?

If you look at the pension ranks, there are six on that list that are in the bottom ten, (#50 being the worst rank). Those six are the topic of the Ghost Bomb Six series. Each of those locations were looked at for information relevant to the spring death surge, their incredible investment gains in 2021, and unexpected mortality after the rollout of the “vaccines.” I make no claim that I have direct evidence that all those things are connected. They just happened in the same location at a certain point in time. You be the judge on what you make of that.

.

Here are those previous posts:

Massachusetts … The Ghost Bomb Six {No.1}

Michigan … The Ghost Bomb Six {No.2}

New Jersey … The Ghost Bomb Six {No.3}

Pennsylvania … The Ghost Bomb Six {No.4}

New York … The Ghost Bomb Six {No.5}

Illinois … The Ghost Bomb Six {No.6}

Now I would like to explore whether there is credible information out there to cause us to consider expanding our list of really bad pensions from 2019/2020 that saw one of these Ghost Bombs go off.

Connecticut?

.

This state did not originally make the series because it was not in the bottom ten of the ALEC rankings. ALEC put it at #35. But like I said, there are other sources of rankings. What do those others say about Connecticut’s pensions back in 2019 or 2020?

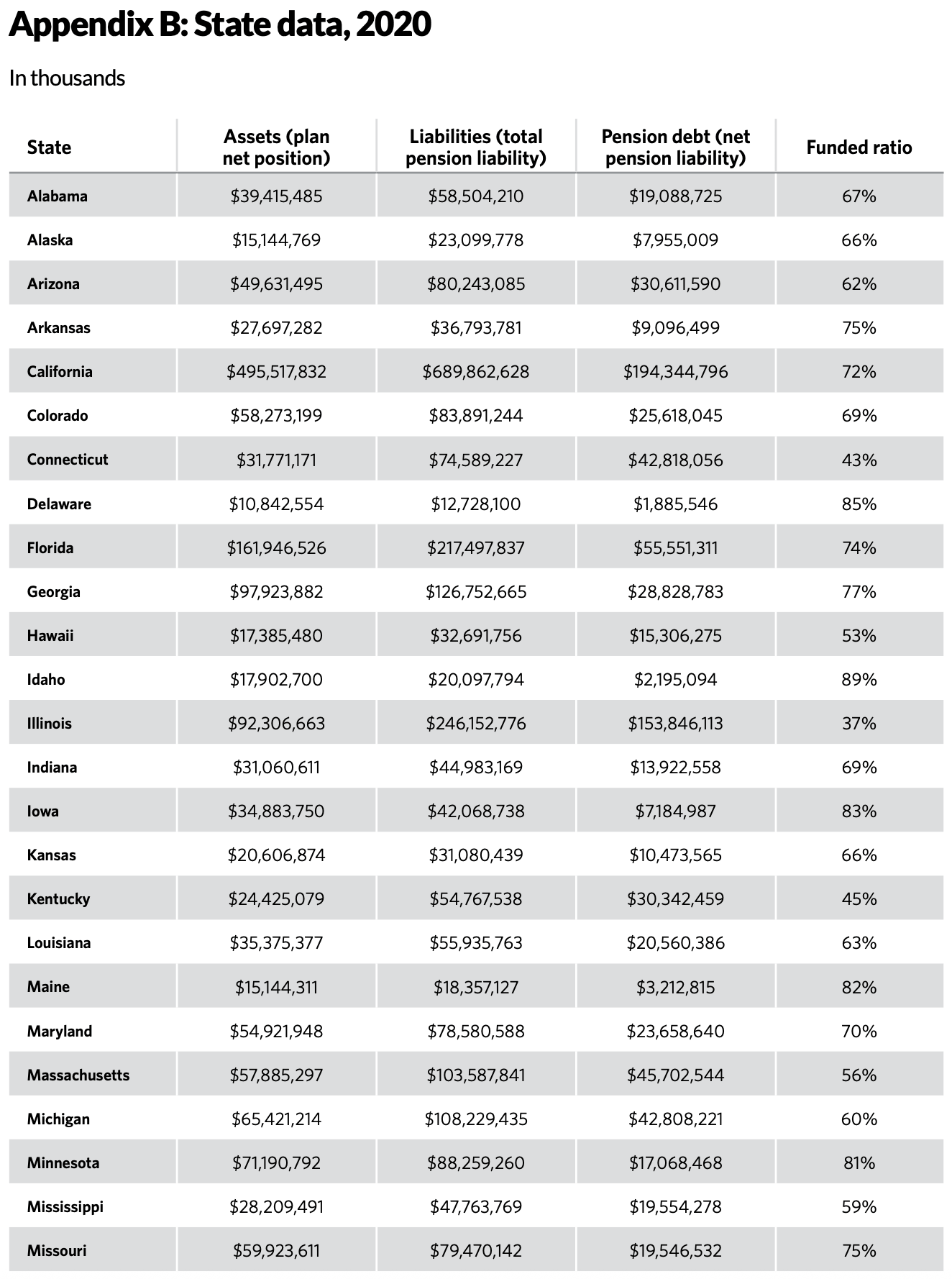

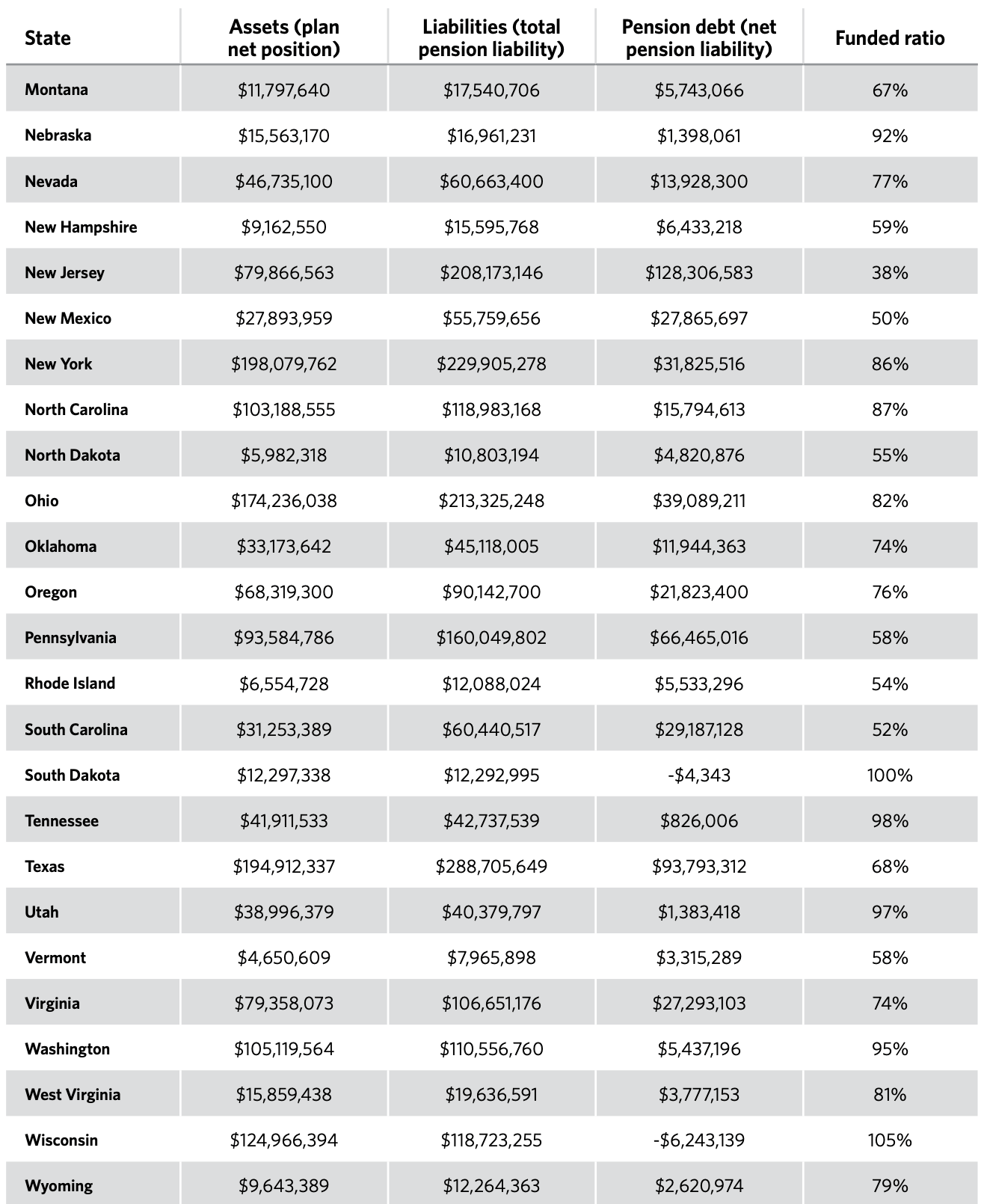

For example, one way to rank a pension is by what its funded ratio is. The funded ratio measures the financial health of a pension system by comparing the assets it has saved to the total benefits it has promised workers and retirees. A higher percentage means the system is better funded, while a lower percentage means a larger gap between what has been promised and what has been set aside.

In this report from the Pew Charitable Trusts from 2022, there is a chart that lists the funded ratio for all the states as of 2020. Connecticut comes in with a 43% ratio. Only Illinois and New Jersey have worse funded ratios - and of course those two are already in the Ghost Bomb Six!

.

(entire list)

.

So right there is one case for a bottom ten entry for Connecticut.

.

But as I mentioned in my last post, there are other sources like Moody’s and the Federal Reserve that can give you some kind of rating for a pension. I will give you here just a little snippet of a discussion on this I just had with my dear friend Chat, (the entire talk will be in the supplemental):

2. Comparison with other analyses

Different organizations use slightly different methods, but they generally place Connecticut in roughly the same range.

Typical positions around 2019–2020:

Source / MethodApproximate ranking

Federal Reserve Z.1 funding ratio~44th = 6th worst

Pew funded ratio comparisons~3rd to 6th worst

Moody’s adjusted liabilities~4th to 5th worst

.

.

.

May 2020

“… Among all plans covering general state government employees, only Kentucky and Illinois had lower funding ratios than Connecticut in 2018.1 These funding estimates likely understate the true shortfall because they are based on assumptions adopted by plan trustees that many economists believe are overly optimistic. The pandemic will likely further weaken plan finances. Stock market losses are eroding plan reserves …”

.

.

.

Come on Connecticut … you’ve got to turn it around!

.

.

.

The Big Payday

12/02/2024

“… “Reaching the 55% funded threshold for SERS is a remarkable achievement considering the 39% funding level in 2020 and the jump from 51% funded to 62% for TRS in the same period,” Office of Policy and Management Secretary Jeffrey Beckham, who serves as the governor’s chief budget advisor, said. “However, Connecticut continues to have one of the worst-funded pension systems in the nation …

… The improved funded ratios are the result of a combination of factors, including strong fiscal discipline, additional contributions from excess revenue and surplus funds, and strong investment performance in recent years.”

.

In that quote above, they reference SERS and TRS. Those are the two largest pension groups in Connecticut:

State Employees Retirement System (SERS)

Teachers’ Retirement System (TRS)

.

(The following information from the State Treasurer covers both in a combined table).

.

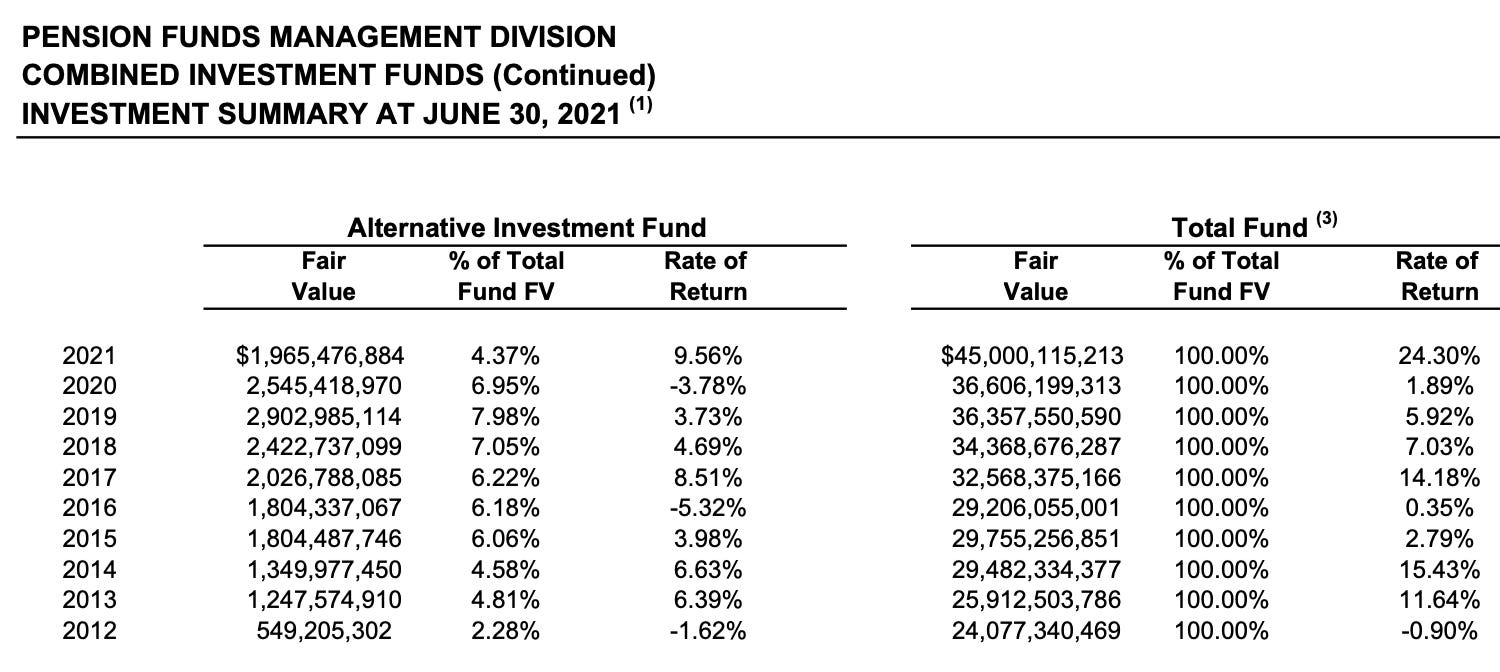

State of Connecticut Treasurer’s 2021 Annual Report

page 172 (PENSION FUNDS MANAGEMENT DIVISION COMBINED INVESTMENT FUNDS (Continued) INVESTMENT SUMMARY AT JUNE 30, 2021)

.

A little closer:

*the year on the top of that list is 2021. Looks like the combined pensions here had the biggest investment returns for quite some time in 2021. Just in the nick of time!

24.30 %!

And around a 9 billion dollar increase from 2020.

.

Nice!

Unexpected Mortality

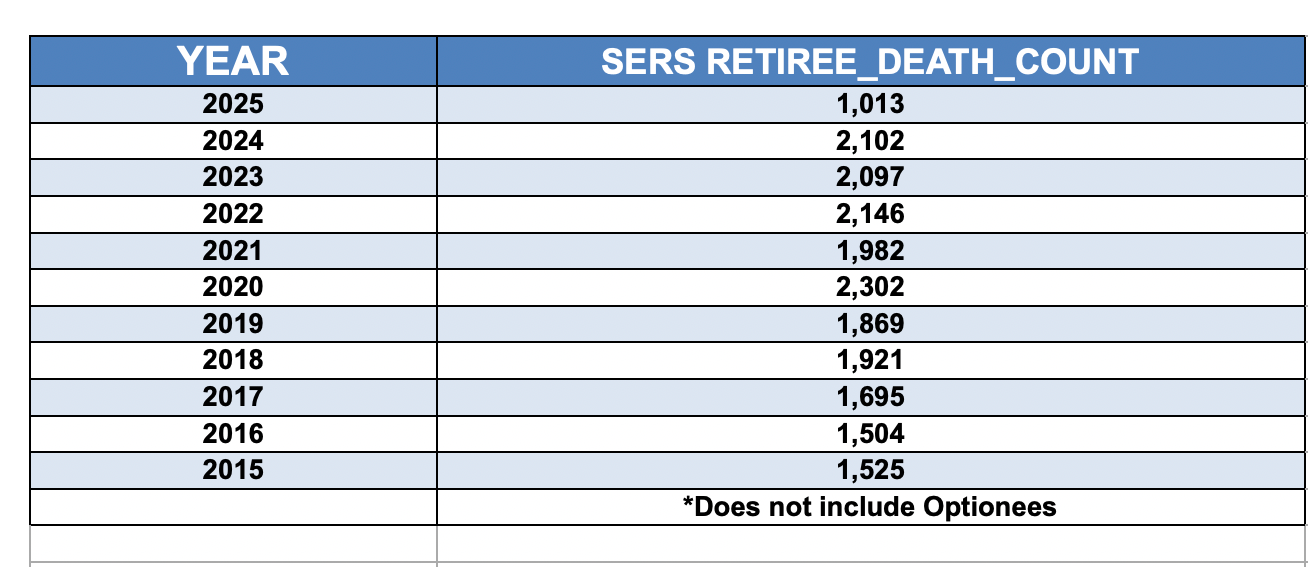

Connecticut is a bit odd in how it reports pension statistics. I found that out the hard way when I did my first look some months ago. Long story short, I had to do a FOIA to the state for the mortality numbers.

Here is what they gave me:

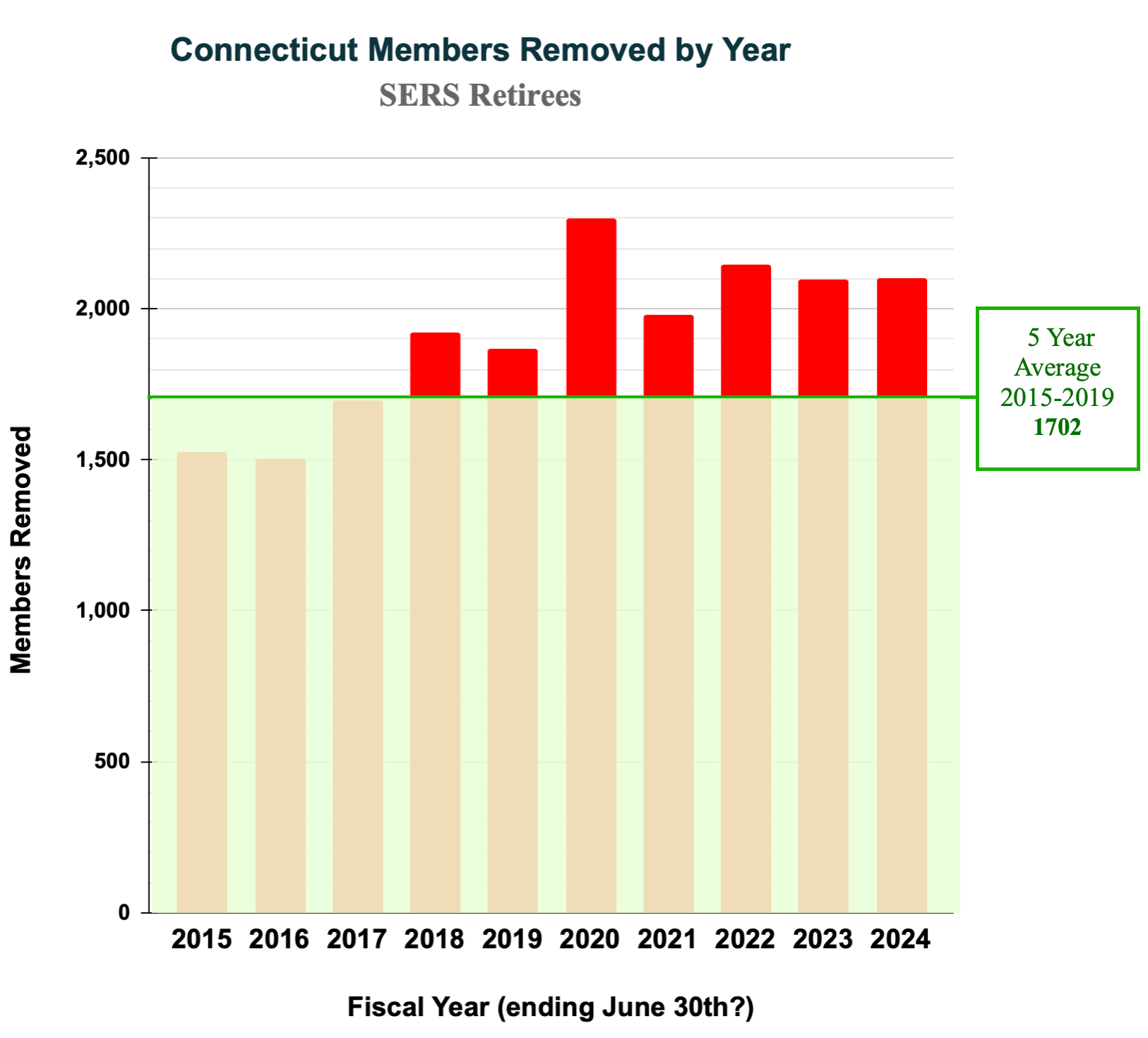

And here is a graph that I produced from that information (they only gave me the SERS numbers for some reason):

.

You can definitely see the evidence of the Ghost Bomb there in that bar for 2020.

But do also take notice of all the elevated bars that follow it, they are all well above the pre-pandemic average.

.

.

.

So I thought I would attempt to track down some mortality data for the other pension system, the TRS. But I ran in to a bit of a roadblock. You see the reason I had to FOIA the state previously was because the annual reports put out by the comptroller simply do not provide any direct mortality numbers.

After chatting up Chat, I have now learned that perhaps such data could be found by looking at actuarial valuation reports for the individual pensions.

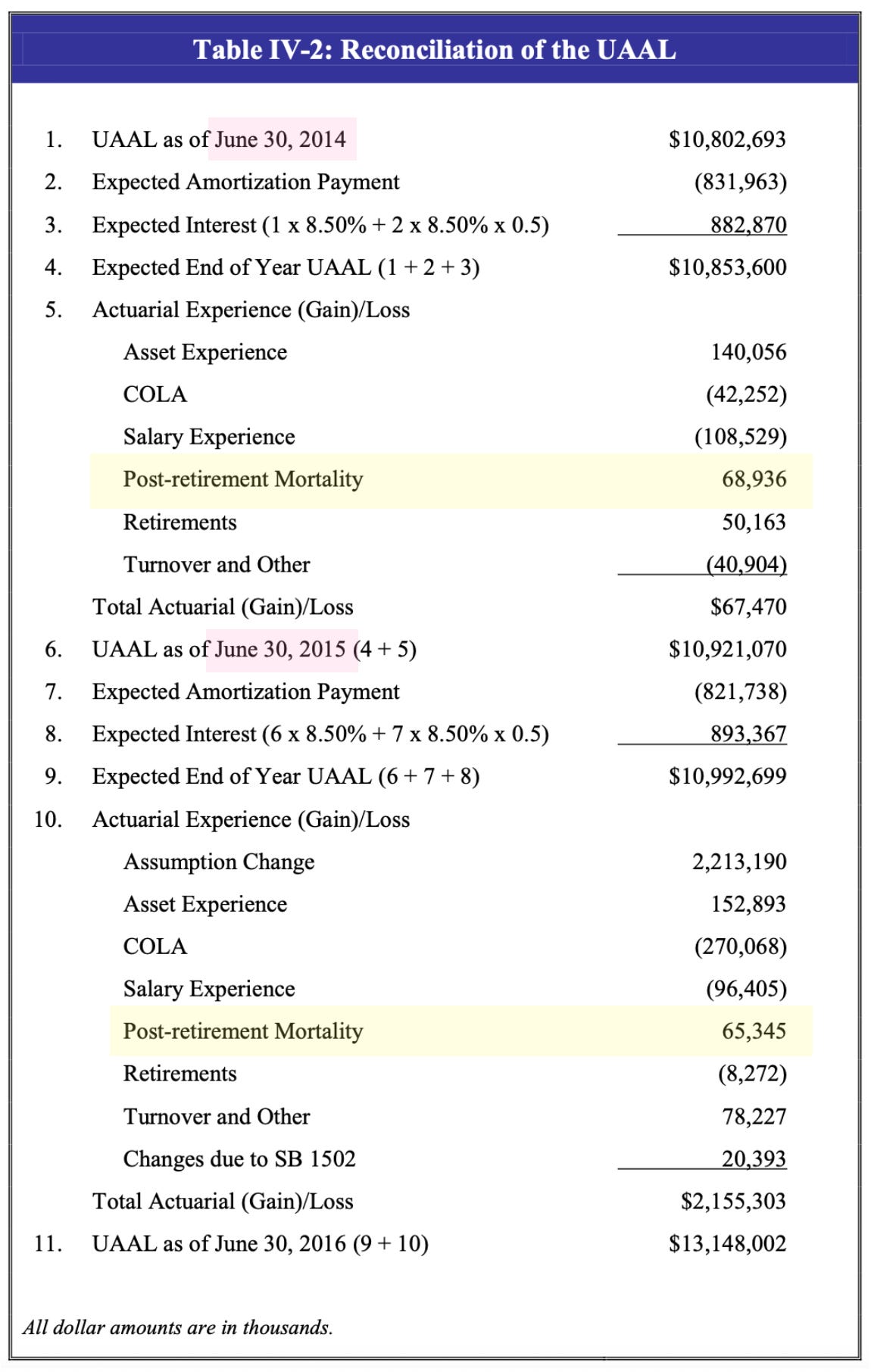

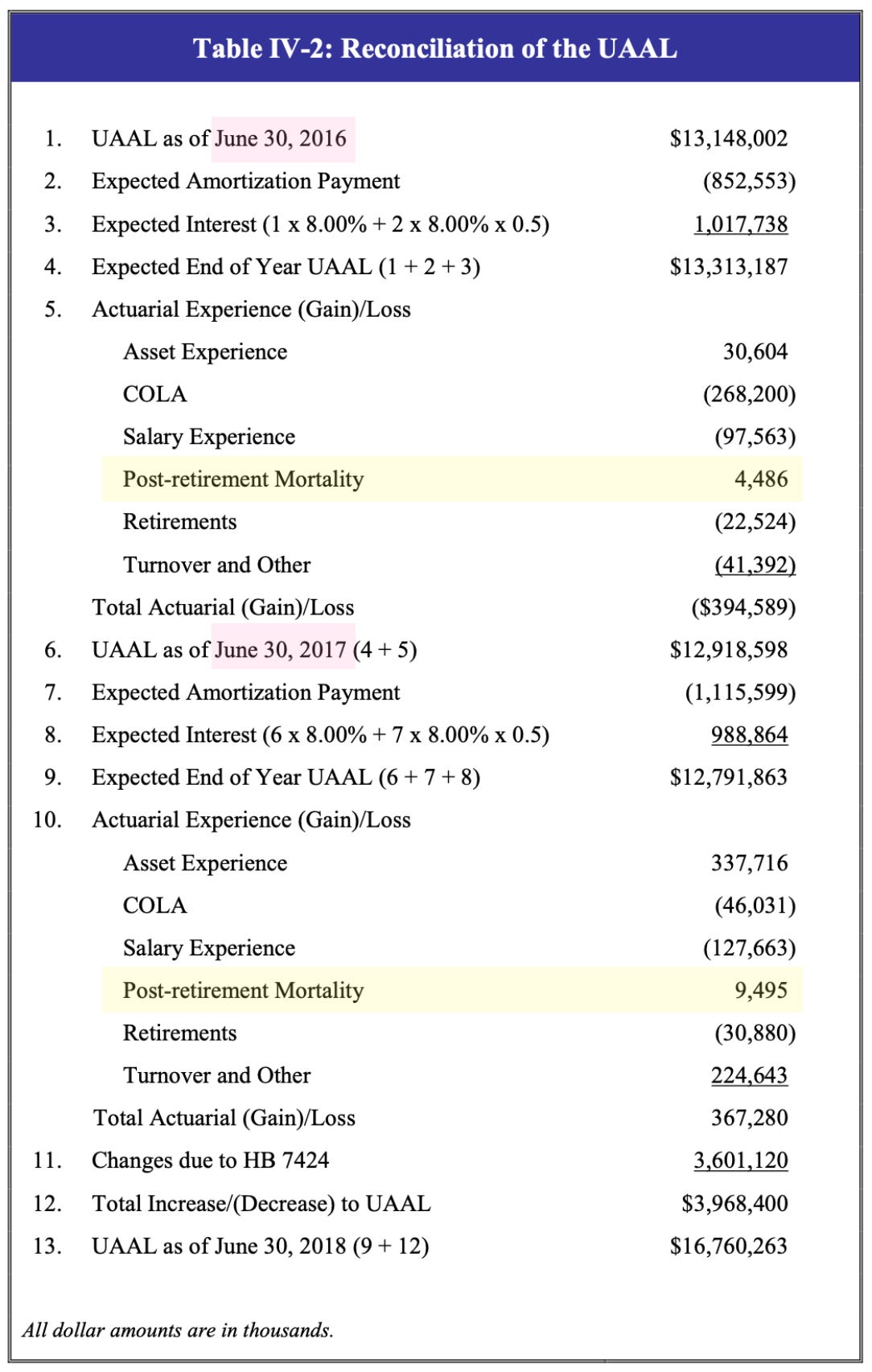

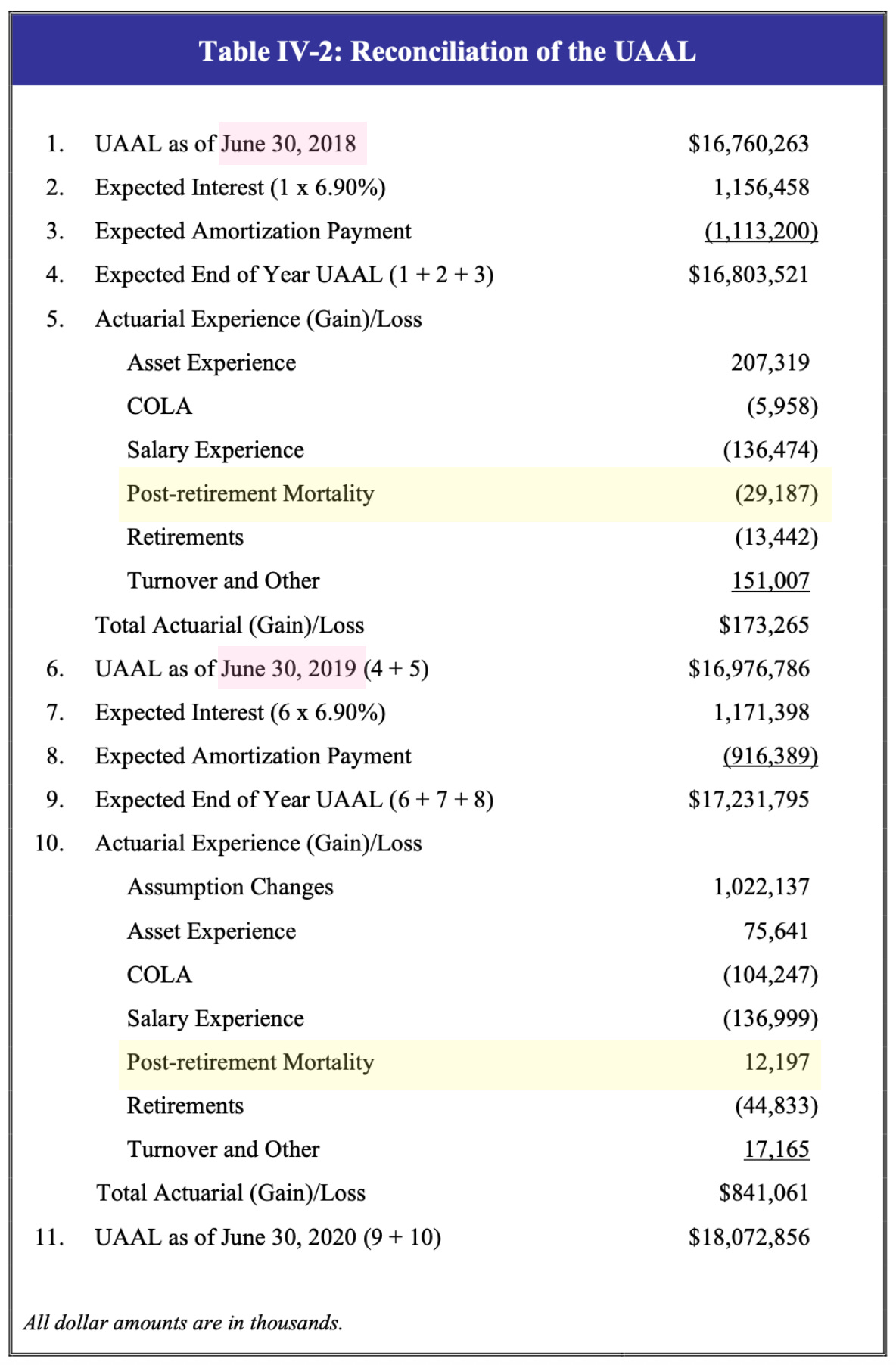

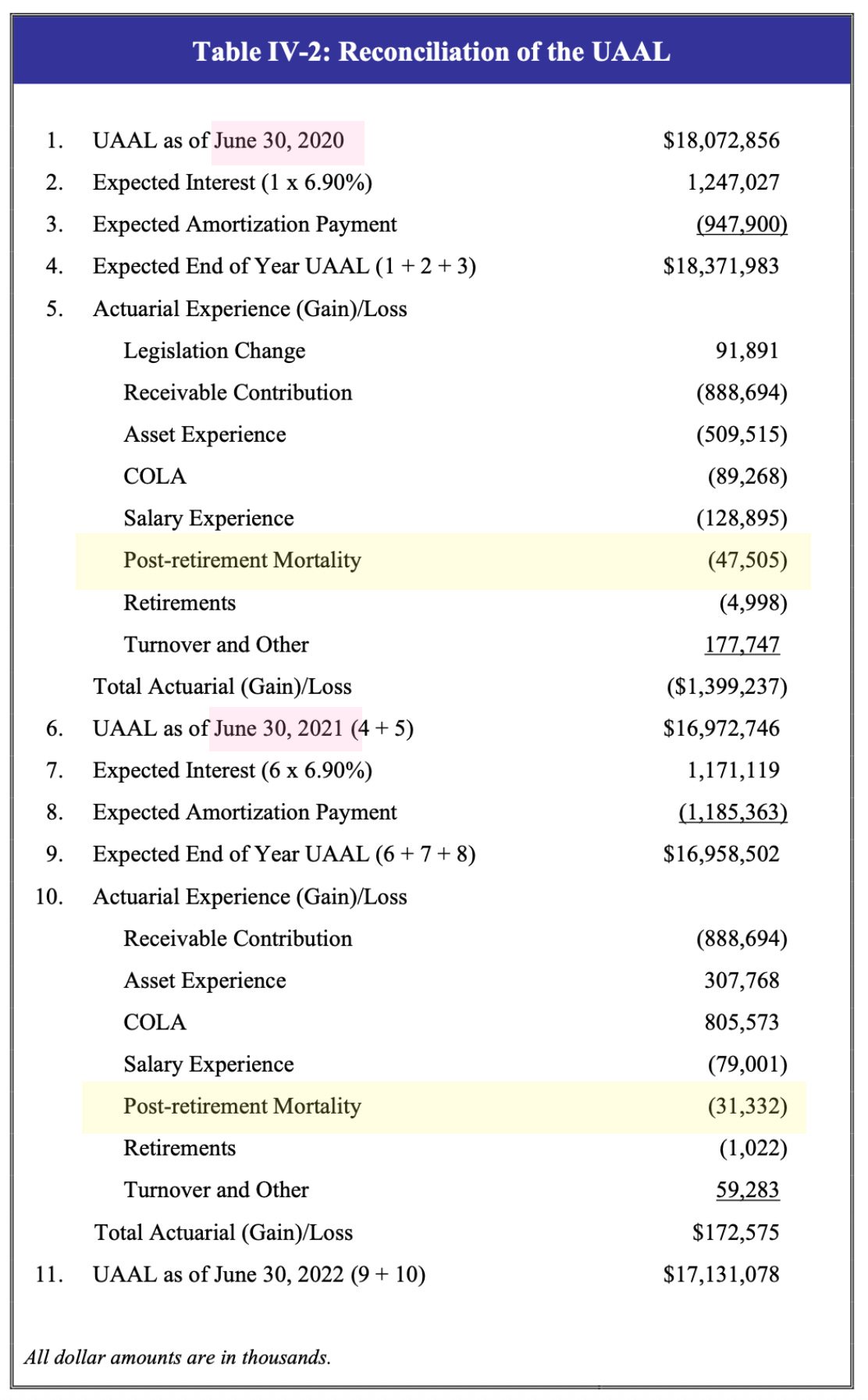

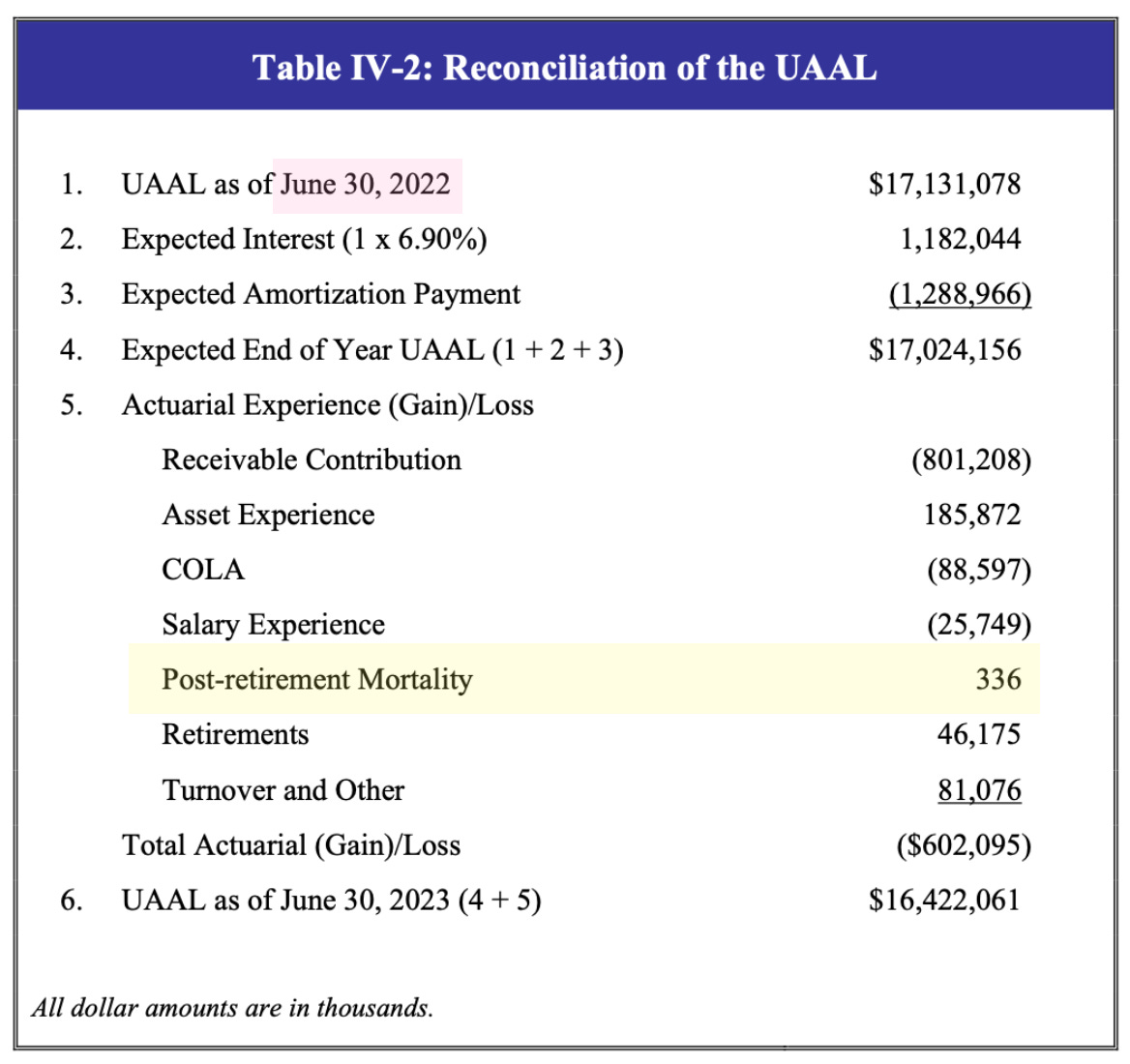

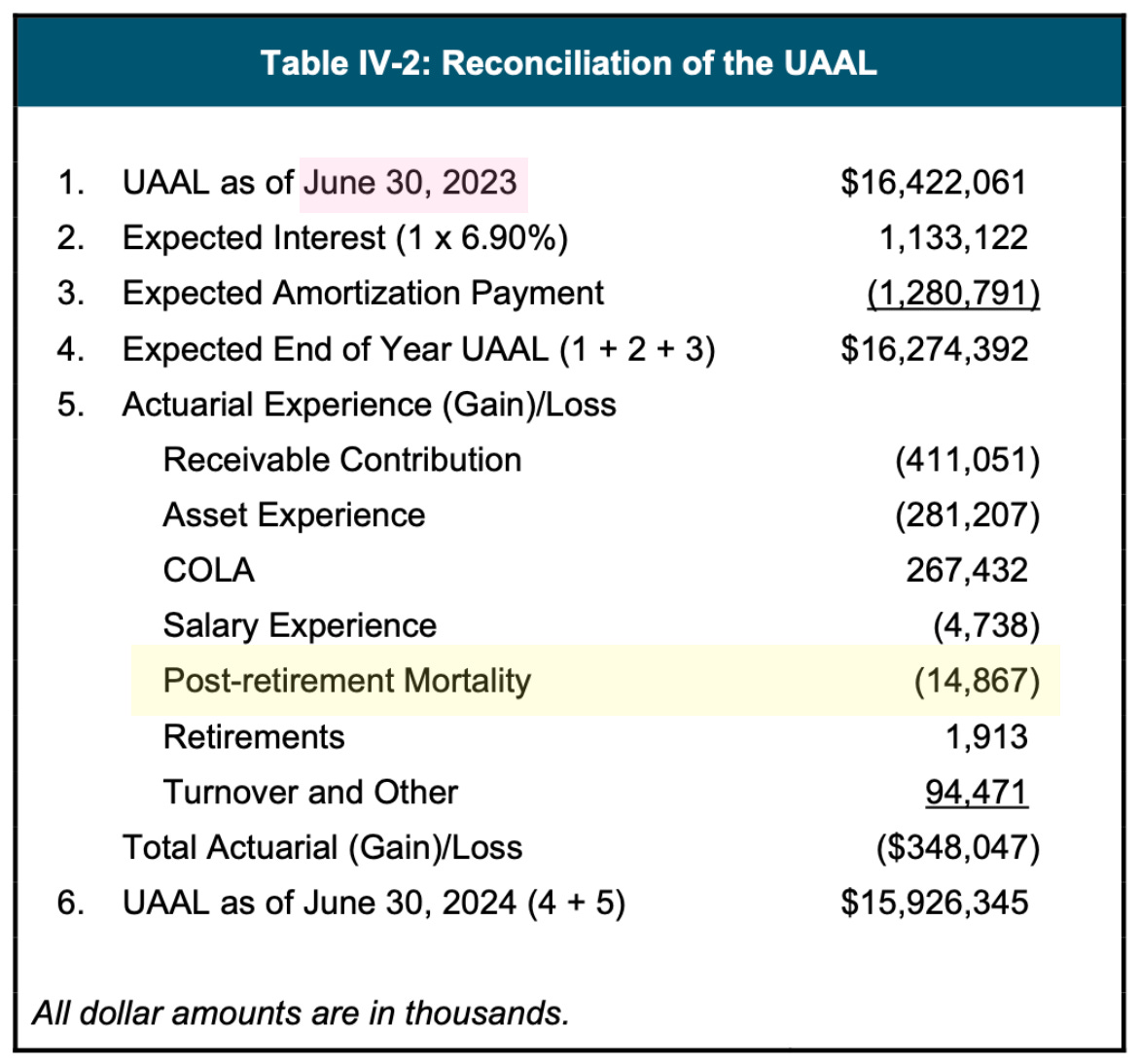

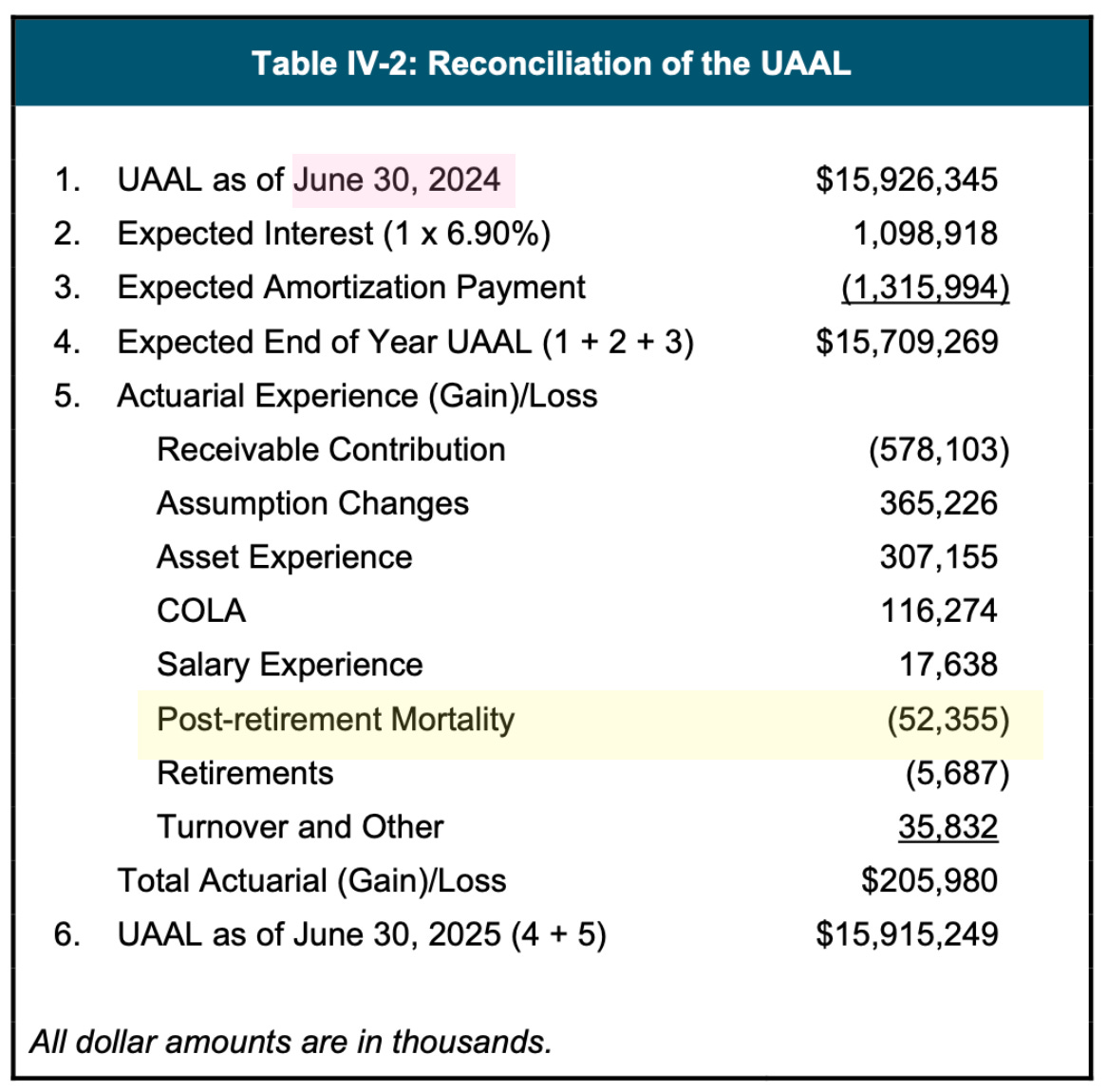

Okay, I went here for those reports. And after some trial and error figuring out that odd numbered years were being lumped in with some of the even numbered years, I think I now have something to show you. I have had to look at individual reports for something called “Reconciliation of the UAAL” … that stands for Unfunded Actuarial Accrued Liability. I am going to reproduce several of these tables now and we are going to look for the line that says “Post-retirement Mortality.” Like I said, some years combine two years into one table, so there will be two lines that say this phrase. After some consult with my good artificially smart buddies, I have come to understand that anything on these tables in parentheses is a “gain” and means the liability decreased. The translation as it relates to “post-retirement mortality” is that more retirees died than expected if that number is in ( ).

(I will put my conversation about that point in the supplemental).

.

.

.

.

.

.

.

.

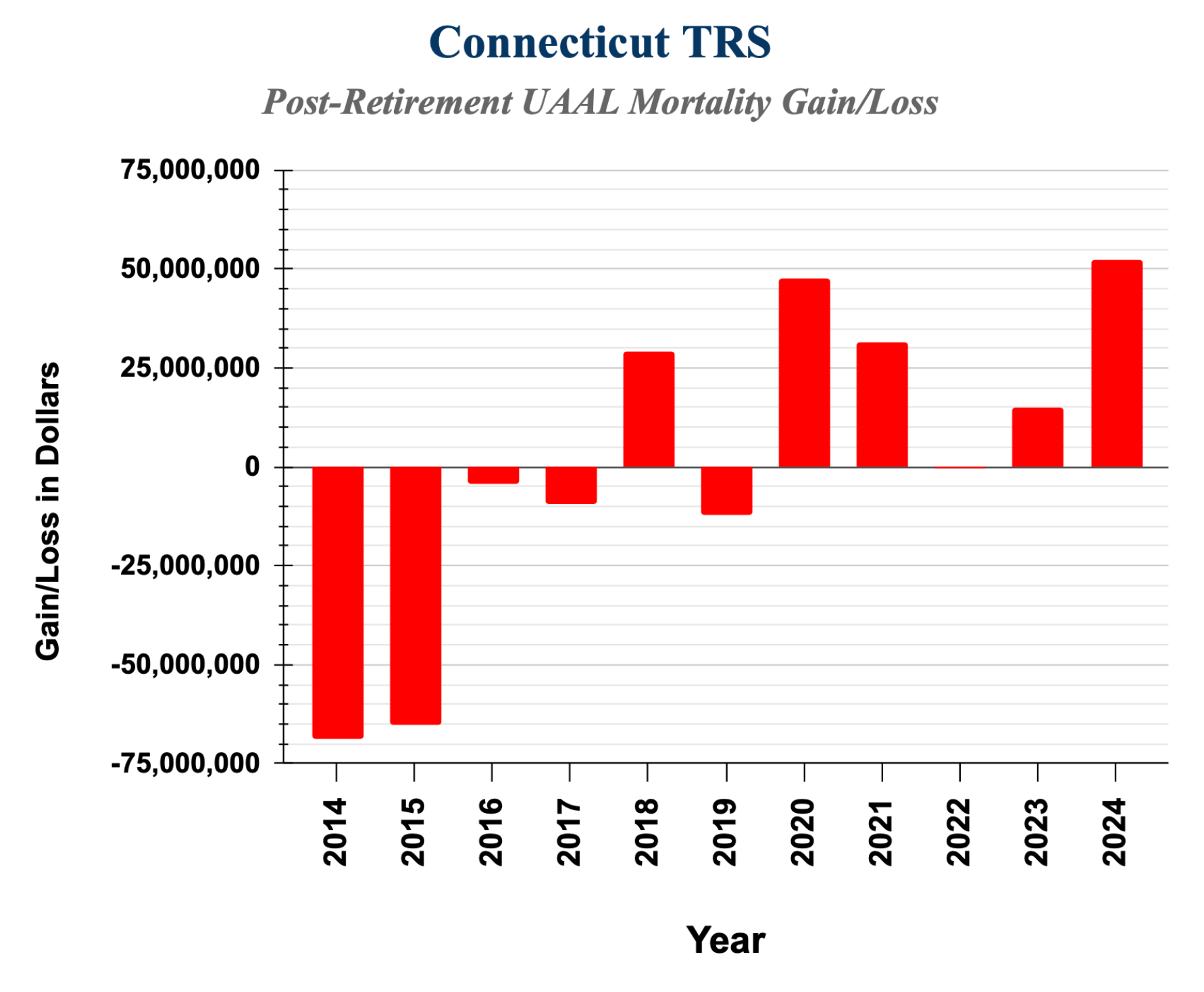

Let me help visualize that for you …

.

Like I said last time, everything hanging down under that 0 line from 2014 to 2019 means that less people died than they expected.

Everything above that 0 line from 2020 to 2024 (*also 2018*) means more people died than they expected.

2020 was bad, you can see the Ghost Bomb there. But I do not like what that is showing for 2024.

.

Not good.

Supplemental

.

ChatGPT discussion on pension rank:

.

My Question: “using the z.1 rating, and the wider considerations, how does Connecticut rank for the time period?”

Using the Federal Reserve Z.1 pension data together with the broader metrics analysts usually consider (Pew, Moody’s, etc.), you can describe Connecticut’s position around 2019–2020 fairly clearly.

1. Z.1 data ranking (structural pension funding)

The Federal Reserve Z.1 Financial Accounts dataset reports state pension assets vs. liabilities and the resulting funding ratio.

For the most comparable period (2018 data used in many 2019 analyses):

Connecticut funded ratio: 36.6%

Rank: 44th out of 50 states (6th worst)

That places Connecticut firmly in the bottom tier nationally, behind most states but slightly ahead of a few with even lower ratios (e.g., Illinois, New Jersey, Kentucky).

Interpretation in plain terms:

Connecticut had about 37 cents saved for every $1 of pension promises.

2. Comparison with other analyses

Different organizations use slightly different methods, but they generally place Connecticut in roughly the same range.

Typical positions around 2019–2020:

Source / MethodApproximate rankingFederal Reserve Z.1 funding ratio~44th (6th worst)Pew funded ratio comparisons~3rd–6th worstMoody’s adjusted liabilities~4th–5th worst

The differences come mostly from different liability assumptions (especially discount rates).

3. Wider fiscal context

When analysts include broader fiscal indicators—such as pension debt relative to income or revenue—the picture remains similar.

Examples cited in research and reporting:

Pension debt relative to personal income: about 8th worst nationally for Connecticut.

Fiscal stability rankings often placed the state in the bottom five to ten overall.

4. Overall assessment for the period

Putting the Z.1 data together with the wider metrics, a fair summary for 2019–2020 is:

Connecticut’s public pension system ranked in the bottom tier nationally—generally between about 4th and 6th worst among the 50 states, depending on the methodology used.

This is why policy discussions at the time often grouped Connecticut with:

Illinois

New Jersey

Kentucky

as states facing the most severe pension funding challenges.

✅ Simple takeaway:

Using the Federal Reserve Z.1 funding ratio, Connecticut was roughly 44th out of 50 states (about the 6th worst)around 2019, and most other analyses placed it in a similar bottom-five range.

.

.

.

Google AI discussion on UAAL “post-retirement mortality”:

.

My Question: “in a uaal table, is a number in parentheses a gain or loss?”

.

In a UAAL (Unfunded Actuarial Accrued Liability) table, a number in parentheses typically represents an actuarial gain or a surplus.

Interpreting the Parentheses

Actuarial Gain: Parentheses indicate a negative UAAL, which occurs when the Actuarial Value of Assets exceeds the Actuarial Accrued Liability.

This is often referred to as a surplus or being “overfunded”.

Negative Value: In standard accounting and finance practice, parentheses are used as a clearer alternative to a minus sign to denote negative numbers.

Since UAAL represents an amount “owed” or unfunded, a negative UAAL (parentheses) means there is no unfunded liability; rather, there is excess funding.

Positive Numbers (No Parentheses): These represent an actuarial loss or an actual unfunded liability, meaning the plan has fewer assets than required to meet its future obligations.

.

My follow up: “in that context, a gain on the UAAL table for “post-retirement mortality” would indicate what? more or less post-retirement mortality?”

.

In that context, an actuarial gain for “post-retirement mortality” indicates more post-retirement mortality than was originally assumed.

Why More Mortality is a Gain

Liability Reduction: In a defined benefit pension plan, the plan’s liability is the present value of all future benefit payments.

Shorter Payout Period: If retirees die sooner than the actuary projected (higher mortality), the pension plan makes fewer monthly payments than expected.

Financial Surplus: This “savings” from fewer payouts reduces the Unfunded Actuarial Accrued Liability (UAAL), which is recorded as an actuarial gain (often shown in parentheses).

Conversely, an actuarial loss in this category would mean retirees are living longer than expected, requiring the plan to make more payments and increasing its total liability.

.

.

*in case you have forgotten …

Pandemic Milestones:

January 20, 2020

-First covid case in the U.S.

December 11, 2020

-Pfizer Emergency Use Authorization

December 18, 2020

-Moderna Emergency Use Authorization

August 23, 2021

-Pfizer full FDA approval

December 2021 / January 2022

-CDC and FDA revise booster recommendations

-Rapid booster uptake

January 31, 2022

-Moderna full FDA approval

August 31, 2022

-FDA authorized Pfizer and Moderna’s new bivalent COVID booster vaccines

April 10, 2023

-Biden declares the end of the pandemic

.

.

.

That’s a lot of work but definitely worthwhile since the conclusion is stunning and not generally recognized. Keep going please.

Wow.

Just...

Stunning.

Thank you!